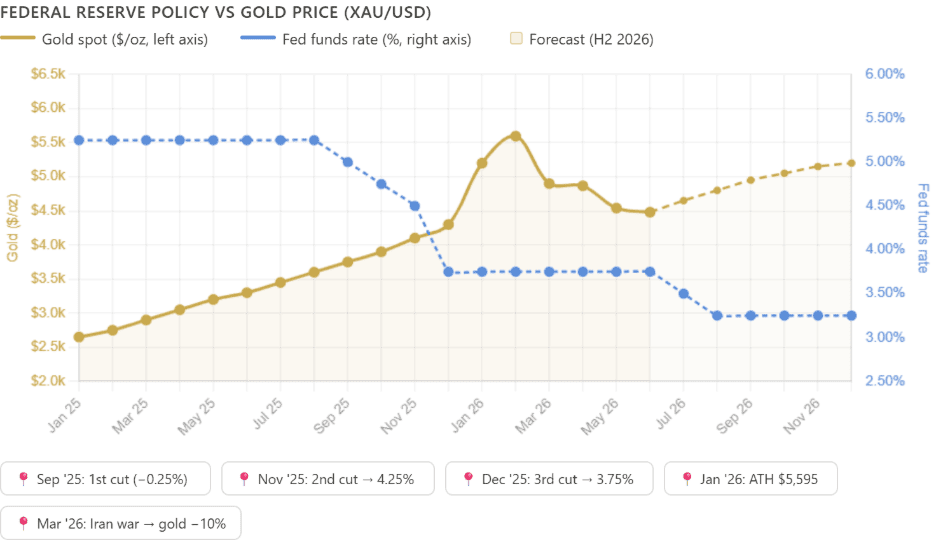

Gold entered 2026 in spectacular fashion, surging to an all-time high of $5,595 per ounce on January 29, 2026 — an extension of 2025's 60%-plus surge, itself the best annual performance since 1979. By the end of H1, however, the picture had changed materially.

Why did gold decrease? The US-Iran military conflict that escalated in late February 2026 proved paradoxically bearish: rising oil prices supercharged inflation expectations, prompting markets to price out Fed rate cuts and even assign a roughly 50% probability to at least one rate hike by year-end. Higher-for-longer real yields strengthened the dollar — gold's twin headwinds. The metal shed more than 10% in March alone, its worst monthly decline since June 2013. Gold rate broke decisively below the key $4,300 support level following the renewed US strikes on Iran and the increased probability of a FED rate hike in September. The gold price predictions were revised down in late June – early July.

Gold price today: Gold spot (XAU/USD) is trading near $4,100, down above 25% from January’s record but still up ~22% year-over-year. The 52-week range spans $3,248 to $5,595, reflecting the extraordinary volatility of the last 12 months.

Gold Forecast & Price Prediction 2026 and Beyond– Key Notes

- Gold forecast 2026: After a 26% correction from January's $5,595 all-time high, gold is consolidating near $4,000. Bank year-end targets now cluster between $4,500 (JPMorgan) and $4,900 (Goldman Sachs) — a recovery, not new record highs, is the consensus for H2.

- BASE CASE (50% probability) — $4,000-$4,700 consolidation/recovery: inflation cools as oil stabilises, the Fed stays on hold, and gold grinds back toward $4,500–$4,900 into year-end, in line with the JPMorgan and Goldman targets.

- BULL CASE (25% probability) — $4,900-$5,200: a durable US-Iran deal reopens the Strait of Hormuz, September hike odds collapse, and ETF flows turn positive. Morgan Stanley and UBS see $5,200; Wells Fargo remains the outlier at $6,100–$6,300.

- BEAR CASE (25% probability) — $3,800-$4,200: the Fed hikes in September (markets price ~60%). Goldman's hike scenario puts gold at $4,400 by year-end, with technical extension toward the $3,800 area.

- Gold forecast 2027: Gold’s 2027 outlook hinges on delayed monetary easing and sustained demand. With Fed cuts now expected in mid-to-late 2027, rate-driven support is postponed but not removed, while central bank buying and physical demand remain strong. Mainstream forecasts cluster between roughly $4,900 and $6,000, keeping a retest of record highs in play if easing resumes.

- Gold forecast for the next 5 years (2030+): Longer term, structural drivers—reserve diversification, fiscal pressures, and low private allocations—continue to underpin the bullish case. Projections for 2030 range broadly from $8,000 to above $10,000, emphasizing that direction matters more than precise targets.

Get more gold sentiment and trading signals, forecasts, and news with NAGA Insights.

With NAGA.com, you can trade CFDs on gold spot (XAU/USD) if you want to speculate on price movements or invest in gold mining stocks or gold mining ETFs.

Fundamental Gold Analysis and Forecast 2026: Should you buy gold at $4,000?

Gold dominated 2025 as the top-performing major asset class, outpacing equities, while gold miners ETFs led leveraged plays. The first half of 2026, by contrast, delivered gold's sharpest correction since 2013 — yet the structural bull case has bent rather than broken: bank targets have come down, but every major institution still expects gold to end 2026 above the ~$4,000 level.

The Iran-War Headwind: Gold's Unusual Dilemma

The US-Iran conflict has created a structurally unusual dynamic: the very event that should trigger gold's safe-haven bid is simultaneously stoking inflation and keeping the Fed pinned at restrictive rates. As one market analyst put it, "Gold needs the war to end to rally — not to escalate." Any credible ceasefire or deal to reopen the Strait of Hormuz would likely remove the oil-inflation headwind, freeing the Fed to resume cutting and the dollar to weaken — a highly bullish combination for gold.

The conflict re-escalated in early July: US forces carried out strikes on targets in Iran over two days in response to attacks on vessels in the Strait of Hormuz, prompting retaliatory strikes on US bases in Kuwait and Bahrain. Crude oil surged 5% in a week. At the same time, President Trump said Iran has reached out seeking a deal, and reports indicate peace talks will continue despite the escalation. Markets are pricing this binary outcome as the single biggest near-term driver of gold direction.

Fed Policy: From Tailwind to Headwind and Back?

The Federal Reserve cut rates three times in late 2025, bringing the federal funds rate to 3.75%. Goldman Sachs had forecast two further cuts (March/June 2026) toward a 3.0–3.25% target. Those cuts did not materialise as Iran-driven inflation repriced expectations. The Fed's preferred PCE inflation gauge rose 4.1% year-over-year in May, the first reading above 4% in three years, and markets now assign ~60% probability to a rate hike in September— a stark reversal. New Fed Chair Kevin Warsh, who succeeded Jerome Powell in May, has offered no forward guidance but reaffirmed the Fed's commitment to controlling inflation — comments markets read as moderately hawkish.

The rate path is now the key variable for gold's H2 direction. Goldman Sachs no longer expects any Fed cuts in 2026, pushing its first projected cut to June 2027 — the main reason it lowered its gold target. Goldman Sachs quantifies that every 50 basis points of Fed easing adds approximately $120 per ounce of price support for gold — support that is now deferred rather than removed. Conversely, an actual hike would raise the opportunity cost of holding non-yielding gold.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

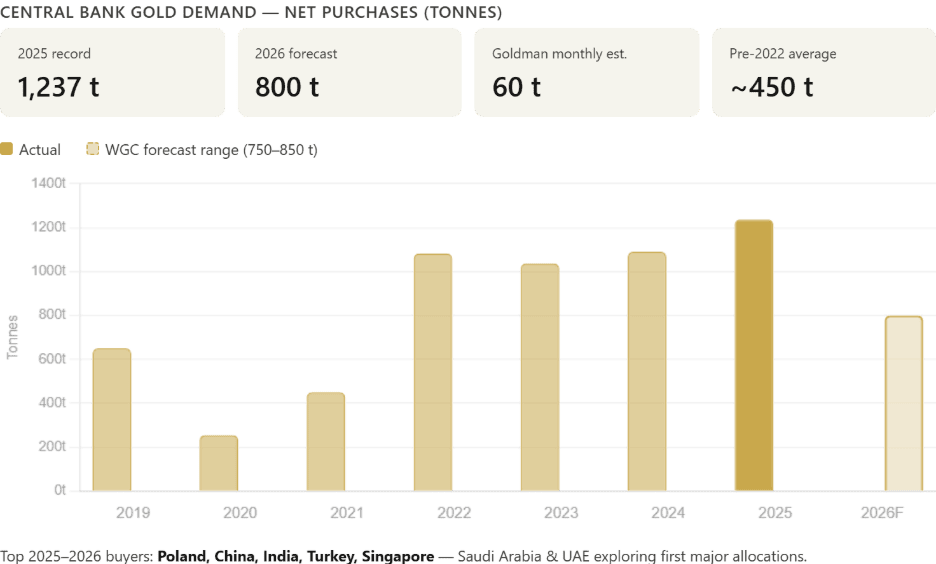

Central Bank Demand: Still Historically Elevated

Central bank gold purchases hit a record 1,237 tonnes in 2025 — the third consecutive year above 1,000 tonnes. The buying has continued through the correction: the World Gold Council reported net official-sector purchases of 41 tonnes in May 2026, and China's central bank posted its largest monthly increase in gold reserves in over two and a half years in June. In OMFIF's annual survey, 45% of central banks say they intend to increase gold reserves within the next 12 months, and nearly 90% expect global official reserves to keep growing.

Forecasts for the full year have been trimmed but remain historically elevated: JPMorgan now expects around 640 tonnes of central bank buying in 2026 (down from 800), while Goldman Sachs continues to model roughly 60 tonnes per month. The World Gold Council projects 750–850 tonnes of official-sector buying for full-year 2026 — below the 2025 record, but still among the top five years since 1971. Leading buyers include China, India, Turkey, Poland, and Singapore. Saudi Arabia and the UAE are reportedly exploring significant allocations for the first time.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

ETF Demand: The Next Catalyst

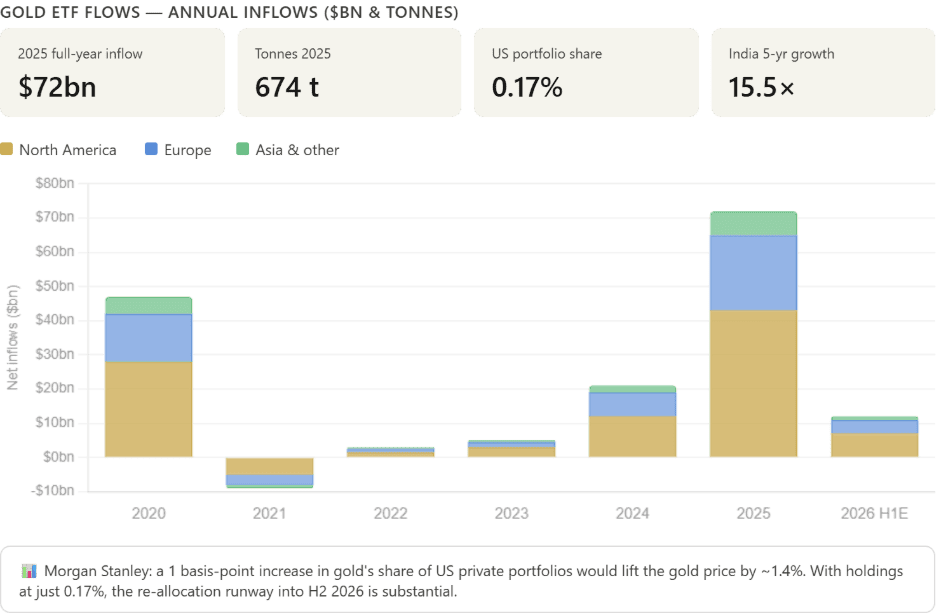

Gold ETFs recorded $72 billion of global inflows in 2025 — a full-year record — led by North America ($43 billion). In 2026, however, ETF flows have become the swing factor — and they have turned negative. Global gold-backed ETFs saw roughly $2 billion of outflows in May, and Asian funds logged their first monthly outflow since August 2025 ($1.2 billion), even as European funds kept attracting money. Fading ETF demand was the primary reason Goldman Sachs cut its year-end target in June.

Morgan Stanley calculates that gold ETFs represent only 0.17% of US private financial portfolios, well below the 2012 peak. Every 1 basis-point increase in gold's share of US portfolios would add approximately $1.4% to the gold price from buying pressure alone. That low starting allocation is why a Fed pivot could flip flows quickly: a meaningful re-allocation back into gold ETFs remains the most credible engine of a Q4 recovery — and its absence is what caps the upside today.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

Supply: Inelastic in the Short Term

Global gold mine supply rose just 2% in Q3 2025 to 977 tonnes, with recycling up 6% to 344 tonnes. While Metals Focus forecasts record mine production and a 6% recycling increase for full-year 2026, supply responses to price changes take years to materialise. Junior mining fundraising hit a record $1.75 billion in October 2025, but new mines won't open before the end of the decade. Supply inelasticity structurally favours the demand side of the gold equation.

Find out more about your gold investing options.

Gold Outlook: Is it worth investing in 2026?

Determining whether it's the right time to buy gold or invest in gold assets depends on various factors, including your financial goals, risk tolerance, and overall portfolio strategy. Gold is trading roughly 26% below its January all-time high of $5,595 — meaning the entry point today is materially more attractive than it was at the start of the year, even as the structural bull case remains intact.

For the right investor, though, the current economic climate and market conditions may present an opportune moment to consider gold as part of a diversified investment strategy. Experts cite three main reasons to consider investing in gold in today's market:

- Gold has a reset entry point with recovery potential: At ~$4,000, gold trades below every major bank’s year-end target ($4,500-$5,200 cluster) but still supported by the same structural pillars that drove the 2025 rally: central bank demand running at 41 tonnes per month in May (per the WGC), ETF holdings well below their 2012 peak, and persistent fiscal deficits driving the debasement trade. A Fed pivot or progress on the US-Iran deal could reignite the move toward bank targets.

- It is often considered a portfolio diversifier: Gold carries no counterparty risk and has historically behaved differently from equities and bonds — tending to hold value or perform differently during periods when other assets have declined. Critically, Morgan Stanley estimates gold represents just 0.17% of US private financial portfolios, well below the 2012 peak. Every 1 basis-point increase in that allocation share would add approximately 1.4% to the gold price purely from demand flow.

- It doesn’t require a lot of capital to start: CFDs on XAU/USD allow exposure to as little as 1/10th of an ounce, making it practical to size a position to your portfolio. Gold ETFs, gold mining stocks, and diversified mining ETFs like GDX also offer accessible, liquid routes in — with no storage logistics. Mining ETFs outperformed gold spot by more than 2× in 2025 (+145% vs +60%), offering leveraged upside if the rally resumes.

However, it's essential to approach gold with a balanced perspective. Gold produces no income — unlike dividend-paying stocks or interest-bearing bonds. Volatility in 2026 is high: the March correction was the sharpest in 13 years, and markets currently price a ~60% probability of a Fed rate hike in September. Gold is best treated as a longer-term position sized appropriately within a diversified portfolio, not a short-term trade.

Gold Technical Analysis & Forecast H2 2026

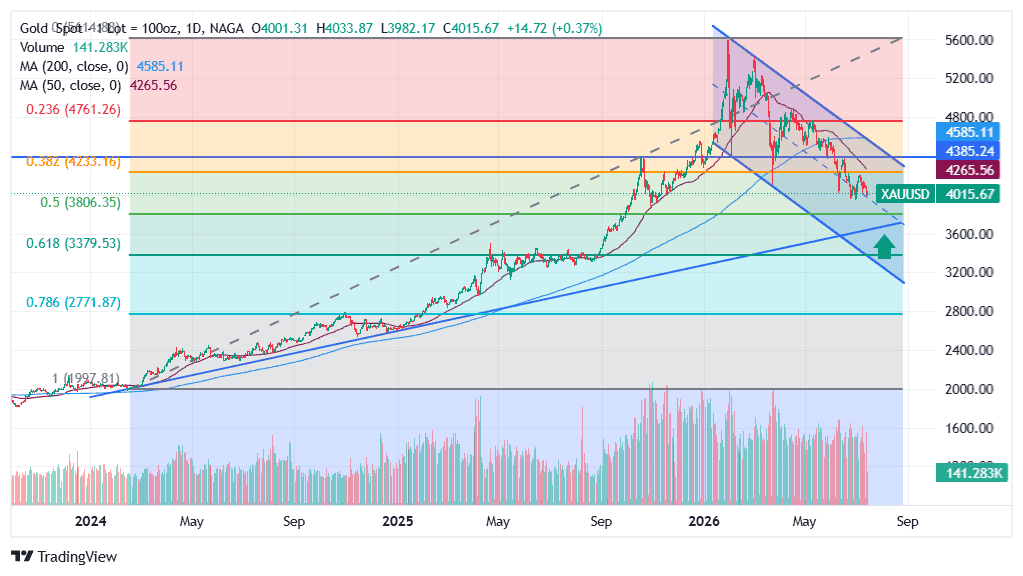

Gold's weekly chart tells a story of an intact primary trend but momentum under severe pressure. After the January blow-off top at $5,595, the price has carved out a descending triangle, with lower highs (∼$5,595 → $4,867 → $4,546) pressing into key support around $4,300–$4,423. Gold broke decisively below the $4,300–$4,320 zone — the 200-day moving average and 38.2% Fibbo retracement, confirming the intermediate trend countrend or secondary reaction according to the Dow Theory. Bears are in control as long as the price remains below the previous support area that now acts as key resistance and within the medium-term descending channel. The MACD is negative and moving sideways; the RSI has room to fall further.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

While $4,000 is the next key support level, psychological and an important floor in recent months, Gold price seems poised to test the critical $3,800 area, a confluence of the long-term trendline and 50% retracement. That area offers the best risk/reward entry for medium- and long-term traders, as a confirmed break below this key support will indicate a change in trend and a bearish outlook.

Gold H2 2026 Technical Levels

LEVEL PRICE TECHNICAL SIGNIFICANCE Near Support $4,060 – $4,100 July consolidation floor; bulls must hold to avoid acceleration Key Support $3,845 – $3,800 Line between consolidation and a deeper correction Bear Extension $3,325 – $3,400 Extended downside target if $3,800 critical support fails ⬤ Current Price ~$4,070 – $4,120 Post-breakdown consolidation; bearish near-term bias Resistance 1 $4,205 Corrective channel top; first bullish objective Resistance 2 $4,300 – $4,320 Former critical support / 200-day zone; close above neutralises the breakdown Resistance 3 $4,500 JPMorgan Q4 target; gateway to the recovery scenario Major Resistance $4,900 – $5,000 Goldman year-end target; psychological round number All-Time High $5,595 January 29, 2026 record; requires macro pivot + ETF re-accumulation

Take your trading to the next level with additional pro-level tools integrated into NAGA and enhance your Gold technical analysis and price prediction:

- TradingView: Access advanced charting, technical analysis, and live market data.

- Trading Central: Get AI-powered trade signals, Economic data, in-depth market analysis, and technical strategy insights.

Will Gold prices rise in the coming days?

Near-term signals are mixed-to-bearish. Gold is capped below $4,546–$4,620 resistance, with the MACD negative and RSI at 48. A bullish reversal requires a daily close above $4,620 alongside a catalyst — most likely progress on the US-Iran ceasefire, softer US payrolls data, or a Fed official signalling resumed rate-cut intentions. If those conditions align, gold could stage a recovery toward $4,730–$5,000 over the following weeks.

Will Gold prices decrease in the coming days?

The short-term downside risk is a break below $4,423–$4,466 support on a hawkish Fed surprise or an Iran escalation (further strikes, suspension of ceasefire talks). LiteFinance's daily model projects gold declining toward $4,370–$3,816 by year-end in the bear scenario. Near-term, the 200-day SMA at $4,340 and the descending channel floor at $4,320 are the critical levels to watch. A close below $4,300 would materially increase the probability of a test of $3,800. Physical buyers from India and China have historically stepped in on dips of this magnitude.

Gold price predictions for 2026 from banks and leading institutions

The bank forecast landscape changed materially in June and July. Most institutions have cut their year-end 2026 targets to reflect the correction, the removal of expected Fed rate cuts, and softer ETF demand — while keeping their long-term structural bull case intact. Here is where the major banks stand as of mid-July 2026:

INSTITUTION YEAR-END 2026 TARGET BIAS KEY DRIVER JPMorgan $4,500 (Q4); $4,300 Q3 avg Neutral, Bullish 2027 Cut ~25% from ~$6,000 on July 3; “range-bound” on softer demand; central-bank floor intact Goldman Sachs $4,900 ($4,400 if Fed hikes) Cautiously Bullish Cut from $5,400 on June 19; no 2026 Fed cuts expected; ETF inflows fading UBS $5,200 (12-month) Bullish Revised from $6,200; expects markets to rethink Fed path; CB buying support Bank of America $4,800 (Q4) Neutral/ Bullish Trimmed on slower investor demand; extreme demand scenario $8,000 by 2027 Deutsche Bank $6,000 Bullish Investor appetite; CB accumulation; muted supply BNP Paribas $6,000 Bullish CB buying (Poland +150 t); gold-silver ratio rising Morgan Stanley $5,200 (H2) Bullish Light investor positioning; diversification building Citigroup $5,000 (3-month target) Neutral Neutral-to-bearish 6–12 month view; flat rather than falling HSBC $4,560 (2026 avg) Neutral Cut from $4,864 in July; 2027 average lowered to $4,925 Wells Fargo $6,100–$6,300 Bull March call unchanged; treats the correction as a buying opportunity Commerzbank Optimistic despite correction Bullish Structural demand is intact despite the recent price fall World Bank +5% for 2026 (target met H1) Neutral Softening CB demand; ETF normalisation in 2027 Forecasts reflect publicly available information as of mid-July 2026. Bank targets change frequently; verify current positions with official sources.

JPMorgan gold price prediction: $4,500 by Q4 after a 25% cut

JPMorgan delivered the most consequential gold forecast revision of the summer. On July 3, the bank slashed its year-end 2026 target to $4,500 per ounce — down roughly 25% from the ~$6,000 forecast it had reiterated as recently as June — and now sees gold averaging $4,300 in the third quarter. The bank attributes the cut to weaker-than-expected demand from key gold-buying sectors and describes the market as “range-bound”, warning that risks tilt further to the downside if strong US data forces the Fed toward rate hikes.

Crucially, JPMorgan has not abandoned the structural gold bull case: it expects central bank accumulation and strengthening physical demand to leave room for further upside into 2027, framing the current phase as consolidation within a multi-year uptrend rather than a reversal.

Goldman Sachs gold forecast: $4,900 — with a $4,400 hike scenario

Goldman Sachs analysts Lina Thomas and Daan Struyven cut the bank's year-end 2026 gold target from $5,400 to $4,900 on June 19. Two pressures drove the revision: fading gold-ETF inflows — including the first monthly outflow from Asian funds since August 2025 — and the removal of all remaining 2026 rate cuts from Goldman's Fed forecast, with easing now delayed to June 2027. If the Fed actually hikes, Goldman forecasts gold sliding to $4,400 by year-end as its appeal as a policy hedge fades; the bank's own vice chairman has flagged September as a live possibility.

Goldman's floor argument rests on sovereign demand: official buyers returned as net purchasers in April, and the bank continues to model roughly 60 tonnes per month of emerging-market central bank buying as reserve diversification continues.

Bank of America gold forecast: $4,800 near term, $8,000 extreme scenario

Bank of America trimmed its near-term gold outlook to $4,800 per ounce for Q4 2026 as investor demand slowed and Fed-related headwinds intensified. Commodity strategist Michael Widmer's longer-term framework is more constructive, resting on three under-appreciated risks: uncertainty around Fed leadership, structural fiscal deficits, and historically low investor gold allocations. In an extreme demand scenario, Widmer has flagged that gold could reach $8,000 by 2027 — the most aggressive published scenario among major banks.

UBS, Morgan Stanley, HSBC — and the remaining bulls

Morgan Stanley targets $5,200 in H2 2026 but is explicit that the call needs ETF inflows to return. UBS also sees $5,200 over the next 12 months (revised down from $6,200), arguing markets will rethink the Fed path as growth cools. HSBC sits at the cautious end, cutting its 2026 average price forecast to $4,560 from $4,864 and its 2027 average to $4,925.

Other institutional gold forecasts for H2 2026

At the other extreme, Wells Fargo has left its $6,100–$6,300 gold target untouched since March — explicitly calling the correction a buying opportunity — and Deutsche Bank continues to hold $6,000. The $1,600 spread between HSBC and Wells Fargo reflects a genuine split: banks that model gold as a rate-sensitive macro asset have cut; banks that model it as a debasement hedge have not.

Gold price predictions for 2026 (AI-Based)

Algorithm-driven models have turned notably more cautious since the July breakdown — and now sit below the bank consensus, a reversal of the usual pattern. CoinCodex's technical model projects XAU/USD ranging between roughly $2,900 and $4,120 for the remainder of 2026, with a bearish year-end bias. The bullish algorithmic calls widely quoted earlier in the year were updated, with Wallet Investor forecasting $4,000 and Coin Price Forecast $5,168 from $7,686 at the end of Q2.

Wallet Investor - Neutral Gold price prediction 2026

Wallet Investor forecasts that gold prices will close 2026 at $3,974.63. Their 1-year gold price prediction is $3,911.12, with the precious metal continuing a sideways trend during 2026.

Coin Price Forecast - Bullish gold price prediction 2026

According to Coin Price Forecast, gold is expected to reach $4,747 by the end of 2026, indicating a potential +18% YTD increase. They also project that gold will hit $5,033 by the end of 2027 and $6,318 by the end of 2028.

Long Forecast - Bearish gold price prediction 2026

According to Longforecast.com, gold prices are projected to experience significant growth over the next few years. For 2026, the platform forecasts gold prices to reach $3,453 by the end of the year, with potential highs reaching $4,216 (the highest gold price target). This upward trend is anticipated to resume, with prices potentially trading above $6,256 by mid-2028.

Gold price prediction for the next 5 years

Long-term structural drivers — de-dollarisation, central bank reserve diversification, fiat currency debasement, and rising emerging-market wealth — remain firmly intact regardless of the near-term Iran-war noise. Here is how major forecasters see gold evolving through 2030:

YEAR WALLET INVESTOR LONG FORECAST COIN PRICE FORECAST 2026 (year-end) $3,974 $3,453 $4,700 2027 $3,855 $5,174-5,770 $5,000 2028 $4,711 $7,313 $6,308 2029 $5,403 $7,973 $7,373 2030 $6,718 $7,881 (Aug 2031) $8,523 Table with AI-driven gold price predictions for the next five years (2026-2030)

Gold price prediction 2030: JP Morgan has separately projected that gold could reach $8,000 per ounce by 2030 in a scenario of continued reserve diversification and sustained fiscal deficits in major economies. Goldman Sachs bases its long-term bullish view on three structural pillars: sustained central bank demand averaging ≈60 t/month, a secular trend toward reserve diversification away from the US dollar, and a structural lack of new mine supply. Historically, gold has risen approximately 7–8% per year over the past 50 years; models based on this compounding place 2030 gold at $9,000–$13,000.

*It is worth keeping in mind that both analysts and online forecasting sites can and do get their predictions wrong. Keep in mind that past performance and forecasts are not reliable indicators of future returns.

When considering gold price predictions for 2026 and beyond, it’s important to keep in mind that high market volatility and the macroeconomic environment make it difficult to produce accurate long-term gold analysis and estimates. As such, analysts and forecasters can get their gold forecast wrong.

What moves the price of gold in the future?

Unlike almost any other asset, gold is typically neither a safety nor a risk asset, though the popular financial media have often called it both over the years (depending on how gold has been performing in recent months). Instead, it’s a currency hedge for which demand rises when there are concerns about inflation diluting the purchasing power of fiat currencies (particularly those most widely held, like the USD and EUR). In other words:

- In times of optimism (aka risk appetite), gold can either appreciate if markets believe growth will lead to inflation, or it can fall if the desire for higher yields overrides inflation concerns and investors move into more classic risk assets, which they believe will provide better returns.

- In times of pessimism (aka risk aversion), gold can either rise if markets believe that stalling growth will lead to rising deficits and/or money printing that could cause inflation, or it can also fall on fears of deflation or a market crash that feeds demand for cash. In times of panic, traders seek cash either to cover margin calls or other obligations or to be ready to go bargain hunting.

If pessimism turns to panic, then gold could either:

– rise if markets are more concerned about the USD or EUR losing their purchasing power than about near-term liquidity needs, as was the case at times from 2009 through 2011.

– fall if markets are more concerned about liquidity than the loss of purchasing power, as was the case in late 2011.

When markets are not concerned about fading purchasing power, the major currencies tend to gain against gold. That can happen due to:

- Low inflation expectations, as we saw starting in late 2011. Concerns about the global economy kept inflation fears low, and so gold began a multi-month downtrend.

- Panic periods are when markets fear a financial crisis, and liquidity becomes the top priority. We saw a gold sell-off during times of peak anxiety about the US or the EU. During these periods, investors tend to sell gold to raise cash.

These are the variables most likely to determine whether gold increases or decreases in the coming days and months:

CATALYST BULL IMPACT BEAR IMPACT US-Iran ceasefire deal Removes oil/inflation headwind; allows Fed to cut; very bullish Failure or escalation → oil spikes further; rate hike bets rise US non-farm payrolls Weak jobs data → Fed cut bets return; gold rallies Strong payrolls → hawkish Fed; dollar strengthens; gold falls Fed decisions (July 29 meeting; September hike priced at ~60%) Dovish guidance revives cut bets A hike raises the opportunity cost of gold Central bank buying pace Goldman expects 60 t/month — ongoing structural floor Any surprise slowdown or selling reduces the demand floor ETF flow direction Re-accumulation → next leg higher; only 0.17% of US portfolios Sustained outflows signal loss of investor conviction US dollar (DXY) DXY weakening → cheaper gold for non-USD buyers Dollar rally → gold headwind US debt/fiscal dynamics Tariff revenue shortfall → more Treasury issuance → gold as a hedge Limited near-term bear case from fiscal alone Table with the main gold rate drivers in H2 2026

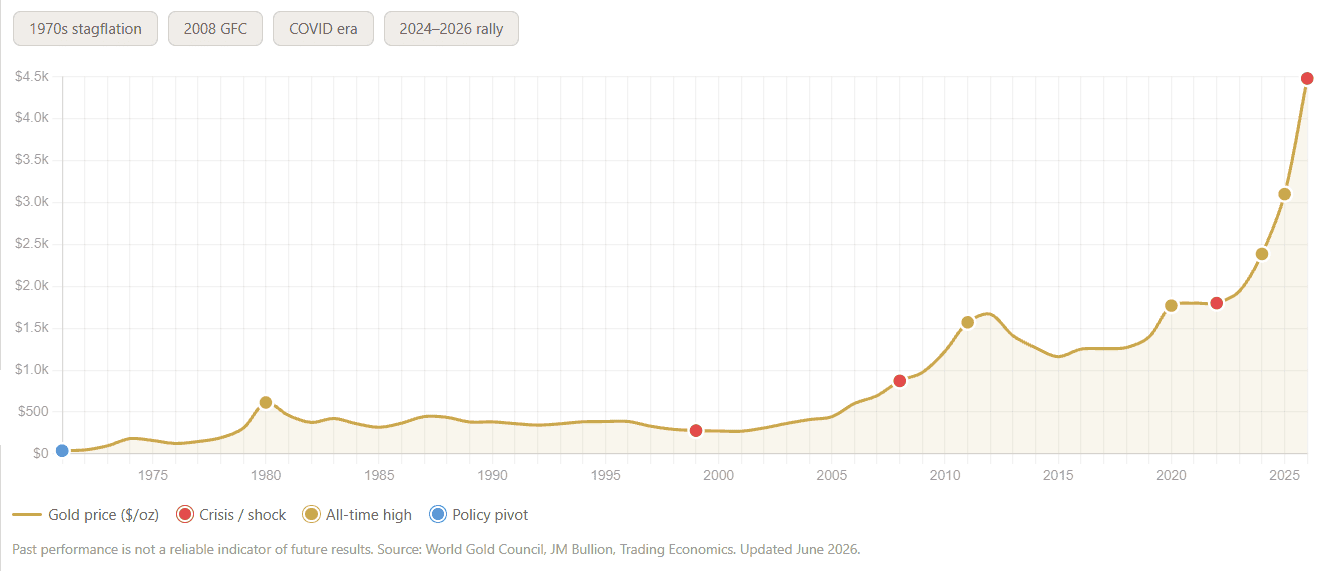

Gold price history: from $35 to $5,595 — the key moments that shaped today's market

Understanding where gold is heading in H2 2026 requires understanding where it has been. Gold was fixed at $35 per troy ounce under the Bretton Woods system until August 1971, when President Nixon ended dollar-to-gold convertibility — the single most important event in the metal's modern history. Every rally since has been a reflection of eroding confidence in fiat currency.

Gold has set its record high price during five distinct eras, each driven by different macroeconomic forces — and the pattern is clear: each successive all-time high has been reached faster than the last. It took 31 years to surpass the 1980 high, 9 years to surpass 2011, 4 years to surpass 2020, and barely a year to surpass 2024.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

1971–1980 — The first great bull market. Nixon's 1971 decision to end Bretton Woods unleashed gold from its $35 peg. Stagflation and geopolitical turmoil pushed gold to $850/oz by 1980 — a record that stood for nearly 28 years. Gold's 1980 peak of $850 equals approximately $3,200 in today's dollars — which means the 2026 highs above $5,000 represent the first time gold has genuinely broken its 1980 record in real, inflation-adjusted terms.

1999 — The 20-year low. Central bank sales and dot-com optimism crushed safe-haven demand. Gold bottomed near $252/oz in 1999 — setting up the greatest buying opportunity of the modern era. Investors who bought near the 1999 low saw roughly 10× returns.

2008 — The $1,000 barrier. Gold first broke $1,000 in March 2008 during the early stages of the Global Financial Crisis as Bear Stearns collapsed and the Fed launched emergency cuts. Gold had traded below $300 as recently as 2001.

2011 — The post-GFC peak at $1,921. US and Eurozone debt crises, combined with QE from the Fed and ECB, pushed gold to $1,921/oz in September 2011. This record has been held for nine years, until the COVID-era rally of 2020.

2020 — COVID pushes gold past $2,000. The macro effect of the COVID-19 pandemic caused gold to establish a new all-time record of $2,075 in July 2020. Near-zero interest rates, trillions in fiscal stimulus, and extreme uncertainty drove the rally.

2022 — The rate-hike bear market. The most aggressive Fed tightening cycle since 1980 — 525 basis points in 16 months — hammered gold back to $1,618/oz as real yields spiked. A reminder that even structural bull markets experience severe corrections.

2025 — The supercycle. Gold broke through $3,000 in early 2025, $4,000 by late 2025, and surpassed $5,000 per troy ounce in early 2026. The catalyst mix was unprecedented: record central bank buying, three Fed rate cuts, the end of quantitative tightening, tariff-driven inflation, and ETF re-accumulation. Gold gained 60% in 2025 alone — its best annual return since 1979.

January 2026 — A new all-time high of $5,595. January 28, 2026, saw gold smash any preconceived notions about its price ceiling, pushing north of $5,400 for the first time — the crest of the wave begun in September 2025. The 2026 price above $5,000 is the first time gold has exceeded its 1980 peak in real terms — representing genuine new price discovery, not simply inflation catching up

March–July 2026 — The correction. The US-Iran conflict's inflationary consequences repriced Fed rate expectations sharply, triggering a 25%-plus correction to the around ~$4,000 level — the sharpest correction since 2013. From a historical perspective, corrections of this magnitude within structural bull markets have consistently proven to be accumulation opportunities: gold fell 33% in 2008 before ultimately tripling, and shed 45% between 2011 and 2015 before the next supercycle began.

From 1971 to 2025, gold's compound annual growth rate has been approximately 8–9%, outperforming inflation (roughly 4% annually) over the same period. However, returns vary dramatically by entry point. The lesson of history is not that gold always goes up in the short term — it is that every multi-year structural bull market has been fuelled by the same forces now in play: fiscal deficits, currency debasement, geopolitical fragmentation, and loss of confidence in the monetary system.

Gold has long reflected global economic and political stress, with its price typically rising during periods of heightened uncertainty. In the wake of the global financial crisis, gold surged past $1,000. During the COVID-19 pandemic, gold prices increased to $2,000. Then, when Trump announced tariffs in April, it surpassed the $3,000 mark. The $4,000 mark was hit during the recent prolonged US government shutdown.

Conclusion: Is Gold a good investment for 2026 and beyond?

Drawing from these expert insights, the consensus for the rest of 2026 is stabilisation and a grinding recovery rather than new record highs. The average gold rate could hover between $4,500 and $4,900 per ounce by year’s end. The path from ~$4,000 to those targets runs through two binaries — whether the Fed hikes in September, and whether the US-Iran conflict de-escalates. However, it’s crucial to note that this remains a forecast. Things can change, and there’s always a level of uncertainty.

For potential gold investors, experts from Morgan Stanley, among others, recommend some gold in a well-balanced, conservative portfolio to protect against inflation diluting the purchasing power of fiat currencies and geopolitical factors. But before you invest in gold, do your homework. Understand the risks and costs of buying and selling gold. And keep a close eye on market trends and conditions.

To sum up: experts can make educated gold forecasts and price predictions, but as with any investment, there's no 100% guarantee.

Trade Gold with NAGA.com

Make sure to create a free demo account on NAGA.com! You will be up to date on interesting updates about Gold as an investment asset, and the user-friendly interface will come in handy if you decide to start trading Gold or any other asset.

Visit NAGA Academy to learn more about trading and investing with our free courses.

Sources:

- https://openknowledge.worldbank.org/bitstreams/9dbf64e4-975f-4905-ab9b-dceb8f285169/download

- https://www.morganstanley.com/insights/articles/gold-price-forecast-rally-into-2026

- https://www.gold.org/goldhub/research/gold-outlook-2026

- https://www.goldmansachs.com/insights/articles/gold-forecast-to-rise-by-the-middle-of-2026

- https://www.federalreserve.gov/newsevents/pressreleases/monetary20250917a.html

- https://www.jpmorgan.com/insights/global-research/commodities/gold-prices