As Egypt moves into 2026, the Egyptian Pound forecast increasingly reflects a shift away from crisis-driven monetary policy toward a more normalized economic environment. By the end of 2025, interest rates are expected to have declined from their historic highs into the low-20% range, creating the conditions for a steadier policy framework in 2026. Rather than further aggressive tightening, the Central Bank of Egypt (CBE) is likely to prioritize maintaining positive real interest rates while supporting economic growth, financial stability, and improved investor confidence — all key elements shaping the Egyptian pound’s outlook.

Looking ahead, the Egyptian Pound prediction for 2026 will depend less on short-term interest-rate adjustments and more on deeper structural and fiscal dynamics. Exchange-rate flexibility, progress on economic reforms, foreign-currency inflows, and Egypt’s ability to sustain external financing will be decisive in determining whether the pound can stabilize after years of depreciation. In this article, we analyze the Egyptian pound’s prospects for 2026 and beyond, combining fundamental insights with technical price forecasts from leading analysts to present a comprehensive USD/EGP outlook through 2030.

Egyptian Pound Forecast & Price Predictions – Key Takeaways

- Egyptian Pound forecast for early 2026: At the beginning of 2026, the Egyptian Pound forecast points to USD/EGP trading in a relatively narrow range around 50–52, reflecting reduced volatility compared with previous years as monetary policy stabilizes.

- Egyptian Pound forecast for 2026: For 2026 as a whole, the Egyptian Pound prediction suggests a gradual weakening, with most technical models from LongForecast and Trading Economics indicating an average trading range near 52–55 USD/EGP, despite occasional short-term corrections.

- Egyptian Pound forecast for 2026–2030: Over the medium to long term, forecasts from LongForecast and WalletInvestor expect USD/EGP to trend higher, potentially reaching 56–60 by 2029–2030 under baseline conditions. More aggressive depreciation scenarios projected by WalletInvestor extend beyond this range, but these remain conditional on negative macroeconomic developments.

Fundamental Egyptian Pound Forecast – 2026 Outlook

As Egypt enters 2026, the fundamental outlook for the Egyptian pound shifts from crisis adjustment to managed stabilization. After losing more than 70% of its value since early 2022 due to repeated devaluations, external financing gaps, and high inflation, the EGP is now operating under a more flexible exchange-rate framework backed by IMF oversight and sizable Gulf support. By 2026, the core assumption among policymakers and rating agencies is no longer a sharp one-off devaluation, but rather a controlled depreciation path aligned with inflation differentials and external funding needs.

From a fundamental perspective, the bias for USD/EGP in 2026 remains upward, but at a slower and more orderly pace than in 2022–2024. Inflation is expected to remain above the Central Bank of Egypt’s target, while interest rates—though lower than their historical peaks—are likely to stay sufficiently high to preserve positive real yields. Combined with elevated public debt, ongoing external obligations, and reliance on foreign inflows, these factors suggest that the pound will continue to face structural pressure. However, strong foreign exchange reserves, IMF program discipline, and continued Gulf investment significantly reduce the probability of a disorderly currency move, anchoring the Egyptian Pound forecast for 2026 around gradual rather than abrupt depreciation.

Inflation & Interest Rates: What Matters for the EGP in 2026

By 2026, inflation is expected to remain structurally higher than the Central Bank of Egypt’s medium-term target, but well below the extreme levels recorded in 2023–2024. Consensus projections from official data and market forecasts point to headline inflation in the low-to-mid teens during 2026, reflecting tighter monetary conditions carried over from previous years, easing base effects, and a more flexible exchange-rate regime. While this represents a meaningful improvement, inflation differentials versus major trading partners are still likely to persist, maintaining underlying pressure on the Egyptian pound.

On the policy side, interest rates in 2026 are expected to be lower than their historic highs but remain elevated in real terms. Following the peak tightening cycle, the CBE is likely to prioritize maintaining positive real interest rates rather than aggressively stimulating growth. Lending and deposit rates are therefore expected to stay relatively high by global standards, helping to anchor capital flows into local debt markets and limit speculative pressure on the currency. For the Egyptian Pound forecast, this implies that while easing inflation and high real yields may slow the pace of depreciation in 2026, they are unlikely to trigger sustained appreciation, reinforcing a baseline scenario of gradual USD/EGP upward drift rather than sharp currency swings.

Trade Balance & Key Sectors: Structural Pressures on the EGP in 2026

Egypt’s trade balance will remain structurally in deficit in 2026, continuing to exert underlying pressure on the Egyptian pound. Despite some improvement since the 2022–2023 currency crisis, the economy still relies heavily on imports of food, fuel, and capital goods, while export growth remains uneven. Although previous currency depreciation has improved price competitiveness, import demand is expected to recover gradually alongside economic growth, limiting the scope for a sustained narrowing of the trade gap.

Key foreign-currency–generating sectors provide partial offsets to these pressures. Tourism continues to be a major source of FX inflows, benefiting from Egypt’s cost competitiveness and diversified visitor base. Suez Canal revenues, while volatile due to regional security risks, remain strategically important, even as traffic fluctuations periodically disrupt inflows. Meanwhile, energy exports have weakened compared with earlier peaks, as domestic demand absorbs a larger share of production, constraining gas export capacity. These sectoral dynamics suggest that while service exports can support the balance of payments, they are unlikely to fully offset Egypt’s structural trade deficit.

For the Egyptian Pound forecast in 2026, this implies persistent but manageable external pressure. As long as export earnings and service inflows remain resilient and are complemented by capital inflows, USD/EGP is likely to adjust gradually rather than abruptly. However, any renewed deterioration in trade conditions — such as higher global commodity prices or prolonged disruption to shipping and tourism — would quickly translate into downside risks for the pound, reinforcing the importance of diversification and export-led growth in stabilizing the currency over the medium term.

Foreign Exchange Reserves & USD/EGP Outlook for 2026

Foreign exchange reserves remain a key anchor for the Egyptian pound heading into 2026. According to the Central Bank of Egypt (CBE), net international reserves were elevated by late 2025, supported by multilateral financing, Gulf investments, and improved FX liquidity. Governor Hassan Abdalla emphasized that these reserves are critical to absorbing shocks, maintaining financial stability, and mitigating abrupt currency swings.

With these reserves, the USD/EGP is expected to follow a gradual depreciation path rather than sharp devaluations. Analysts and CBE-guided projections suggest:

- Early 2026: USD/EGP around 51–52 EGP/USD, reflecting carry-over effects from late 2025 FX pressures.

- Mid 2026: USD/EGP likely at 52–53 EGP/USD, as controlled inflation (~10.5%) and high interest rates (21–22%) continue to attract capital inflows.

- End of 2026: USD/EGP forecasted near 53–54 EGP/USD, assuming fiscal discipline, continued IMF support, and stable foreign reserves.

As Governor Abdalla noted, maintaining strong reserves and disciplined monetary and fiscal policies will anchor the pound, making this gradual, fundamentals-driven depreciation scenario the most plausible. Any sharp erosion of reserves or external shocks could push USD/EGP higher than this baseline, but under current policies, the pound’s stability is reinforced.

Egyptian Pound Forecast – Technical (2026 Outlook)

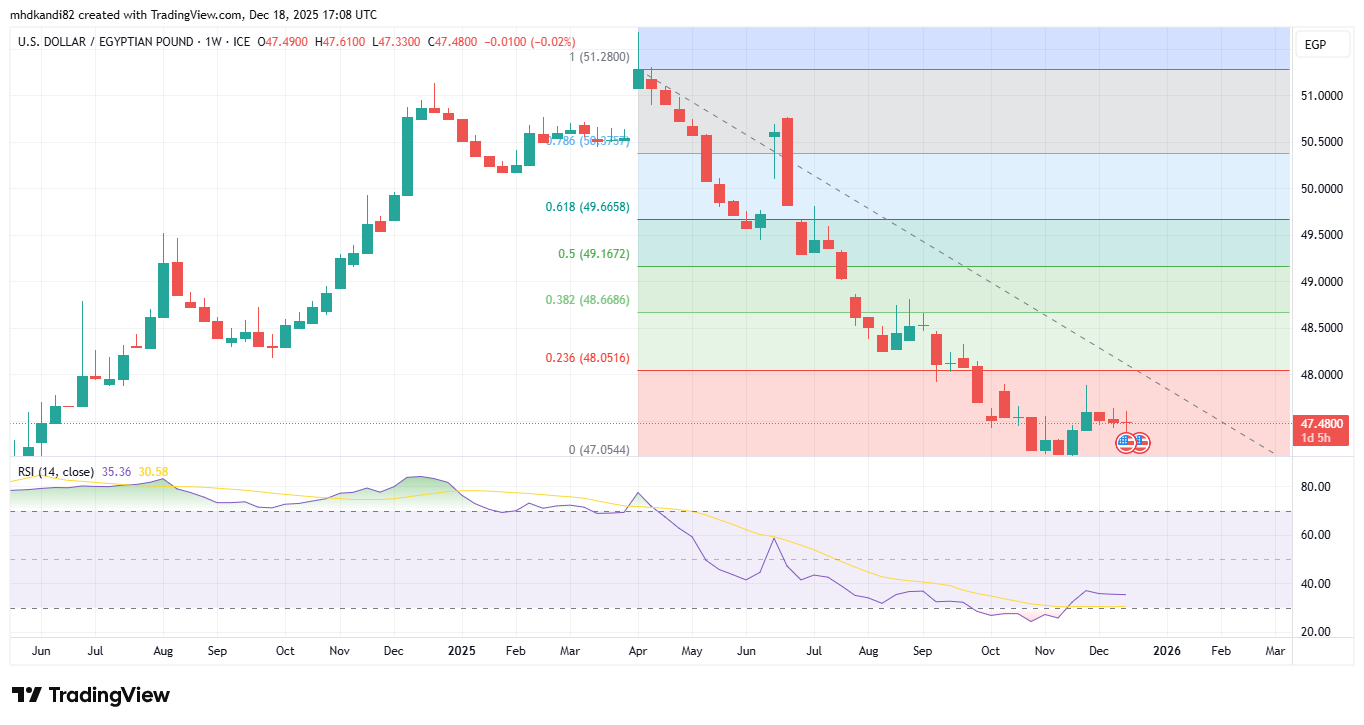

The USD/EGP pair has been trading in a consolidation-to-bearish pattern since mid-2025, hovering near 48.10–48.35. The broader trend remains cautiously bearish, as prices continue to trade below the descending trendline that has limited recovery attempts over the past months.

For illustrative purposes only. Past performance is not indicative of future results.

From a Fibonacci perspective, the pair remains below the 50% retracement at 50.22, with the 38.2% level near 49.34 acting as immediate resistance. On the downside, support lies around 47.90, with a break potentially exposing the 47.10 region.

Momentum indicators suggest muted upside potential. The Relative Strength Index (RSI) sits near 37–38, indicating bearish momentum while approaching oversold territory. A stabilizing RSI above 40 could hint at a potential bullish divergence if USD/EGP holds current support levels.

Key resistance levels for 2026 are 48.80, 49.30, and the psychological 50.20 zone. A decisive move above these could shift momentum upward toward 50.80, while failure to defend support at 47.90–47.10 may trigger renewed selling pressure.

Overall, technical indicators point to continued consolidation with bearish bias in the near term. Traders should monitor RSI trends and price action near support for early signs of potential reversals or further downside continuation.

Egyptian Pound Price Predictions

As 2026 unfolds, the Egyptian Pound forecast is grounded in observable fundamentals and official projections rather than speculation. After years of elevated inflation and tight monetary policy, several key data points shape the Egyptian Pound prediction for the medium term:

Inflation Outlook

Egypt’s annual headline inflation is projected to continue its downtrend into 2026, averaging around 10.5 % for the year, reflecting easing price pressures from food and energy sectors and ongoing disinflationary policies. This is closer to—but still above—the Central Bank of Egypt’s (CBE) target of 7% (±2 pp) by the fourth quarter of 2026.Interest Rate Path

The Monetary Policy Committee (MPC) kept key rates steady in late 2025, with the overnight deposit at 21.00 %, lending at 22.00 %, and main operation/discount rates at 21.50 %. This cautious stance balances ongoing disinflation with financial stability, while longer-term projections suggest rates could ease toward ~16 % in 2026 and ~14 % in 2027 if inflation continues to decline.Foreign Exchange Reserves & Fiscal Support

Egypt’s net international reserves stood at about $47 billion by late 2025, supported by Gulf investments — including a $35 billion UAE deal — and IMF/multilateral financing. Governor Hassan Abdalla noted that these reserves, together with disciplined fiscal policies, provide a buffer against external shocks and help sustain a gradual USD/EGP depreciation in 2026, while covering annual external debt service of over $30 billion.

Central Bank & Expert Signals

The Egyptian pound’s near-term outlook is heavily influenced by the CBE’s cautious monetary stance and the projections of international analysts. Ongoing inflation trends and policy signals will be key in shaping USD/EGP movements through 2026.

The CBE’s MPC (20 Nov 2025) signals a cautious “wait-and-see” approach to monetary easing, as inflation remains exposed to global and domestic risks such as energy prices and services inflation. International analysts, including those polled by Reuters, also foresee inflation continuing to fall through 2025–2026, with annual rates easing toward the mid-teens by mid-2026. Rating agency Fitch Ratings supports the view of a gradually declining inflation environment in 2026, albeit with sticky components, especially in services.

Implications for USD/EGP Forecast 2026

These fundamental indicators suggest a managed depreciation path for the Egyptian pound over 2026 rather than abrupt currency shocks:

Inflation above target but easing: Sustained but falling inflation (from ~12.5% in late 2025 to ~10.5% in 2026) implies persistent nominal depreciation pressure on USD/EGP. Elevated real interest rates initially: High policy rates (around 21–22%) into early 2026 support foreign capital inflows, tempering rapid depreciation, while gradual rate declines may increase near-term volatility. External financing and policy credibility: Continued IMF engagement and cautious fiscal consolidation underpin confidence, making extreme depreciation less likely barring external shocks.

Overall, the Egyptian Pound prediction for 2026 is biased toward gradual, fundamentals-driven weakening rather than sharp devaluation. If inflation continues its downward trajectory toward the CBE target by late 2026 and interest rates ease as suggested by models, the EGP is more likely to depreciate at a measured pace in line with macro trends through the decade.

Egyptian pound to US dollar price forecasts based on algorithms and artificial intelligence for 2026 - 2030

Although the Egyptian Pound has experienced periods of volatility against the US Dollar in recent years, agencies and AI-based forecasting platforms remain cautiously optimistic that the currency will follow a gradual depreciation path through 2026–2030, with moderate monthly fluctuations and potential stabilization supported by fiscal reforms, foreign inflows, and Central Bank of Egypt policies.

Wallet Investor – Neutral USD/EGP prediction 2026–2030

Wallet Investor projects a gradual weakening of the Egyptian pound, with the USD/EGP pair likely to trend from ~48.2 EGP/USD in 2026 toward ~54 EGP/USD by 2030. The platform notes moderate volatility, suggesting potential opportunities for long-term investors if structural reforms and capital inflows continue.

CoinCodex – Bullish USD/EGP prediction 2026–2030

CoinCodex anticipates the USD/EGP exchange rate to gradually rise over the medium term. Their models estimate 47.5–48.5 EGP/USD in 2026, increasing toward ~55 EGP/USD by 2030, reflecting a combination of short-term corrections and long-term depreciation pressures.

LongForecast – Bullish USD/EGP prediction 2026–2030

LongForecast’s algorithmic projections indicate moderate depreciation in 2026 with the pair around 48–49 EGP/USD, followed by a steady upward trend to mid-50s in 2029 and ~60.6 EGP/USD by 2030. These forecasts are derived from statistical models incorporating inflation, fiscal policy, and external debt dynamics.

Trading Economics – Neutral to bullish USD/EGP forecast 2026–2030

Trading Economics’ global macro models suggest the USD/EGP could start ~48.2 EGP/USD in 2026, with gradual increases over the next five years, potentially reaching ~56–57 EGP/USD by 2030, depending on inflation trends, FX reserves, and fiscal stability.

*It is worth keeping in mind that both analysts and online forecasting sites can and do get their predictions wrong. Keep in mind that past performance and forecasts are not reliable indicators of future returns.

When considering Egyptian pound price predictions for 2026 and beyond, it’s important to keep in mind that high market volatility and the macroeconomic environment make it difficult to produce accurate long-term Egyptian pound analysis and estimates. As such, analysts and forecasters can get their Egyptian pound forecast wrong.

Other Forecasts and Price Predictions

Final words on the Egyptian Pound Forecast

If you are considering the Egyptian pound forecast to guide your trading or investment decisions, remember that no projection is guaranteed. Both analyst views and algorithm-based models are subject to uncertainty, as unexpected shifts in policy, inflation, or global markets can quickly alter the outlook. Forecasts should therefore be seen as potential scenarios rather than definitive outcomes.

For that reason, it is essential to carry out your own due diligence. This includes monitoring the latest economic data, reviewing policy announcements from the Central Bank of Egypt, and applying both fundamental and technical analysis to your strategy. Analyst commentary and expert opinions can provide context, but ultimately, your trading decisions should be based on a balanced assessment of risks, objectives, and market conditions. Never invest funds you cannot afford to lose.

Free Resources

Before you start trading Forex, consider using the educational resources we offer like NAGA Academy or a demo trading account.

- NAGA Academy has lots of trading courses for you to choose from, and they all tackle a different financial concept or process – like the basics of analyses – to help you to make more informed trading decisions.

- Our demo account is a suitable place for you to learn more about leveraged trading, and you’ll be able to get an intimate understanding of how CFDs work – as well as what it’s like to trade with leverage – before risking real capital.

Sources: