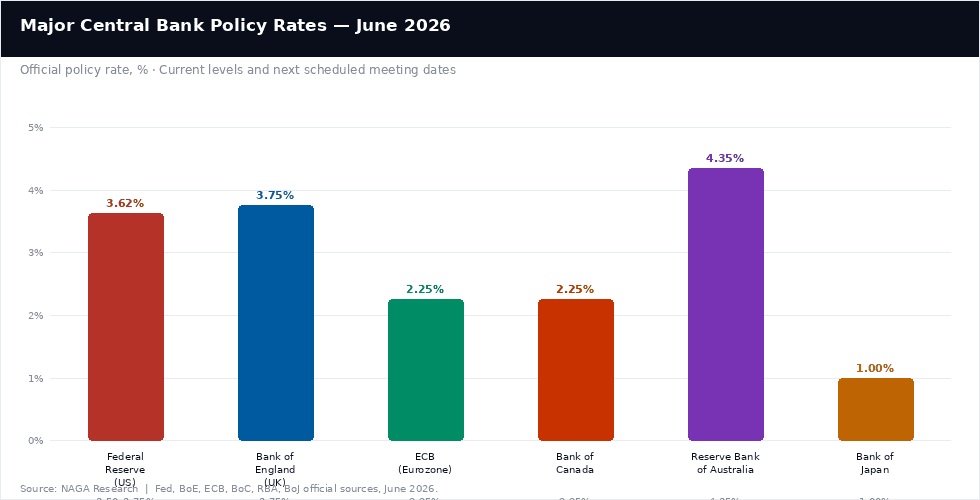

The global interest rate picture in mid-2026 is fundamentally different from where it was 18 months ago, and not in the direction most economists expected. From mid-2024 through early 2025, the world's major central banks coordinated to ease. Then the Strait of Hormuz conflict — which began in late February 2026 — sent oil above $125 per barrel, reignited energy-driven inflation in virtually every major economy and broke the consensus apart.

The result is a fragmented global policy landscape heading into H2 2026: the ECB and BoJ are tightening; the Fed is paralysed between inflation hawks and a political mandate to cut; the BoE is on hold with two members already voting to hike; the RBA is pausing after three hikes; and only Canada holds steady with a bias toward eventual easing if its trade-war-damaged economy worsens further.

The key question for the rest of 2026 is not "will interest rates go down globally?" — in most cases they will not, or not materially. The question is which central bank breaks from the current higher-for-longer consensus first, and what data would trigger that shift.

Interest Rates Forecast 2026 — Key Notes

- US Interest Rate forecast: US interest rates are not expected to go down in the base case for 2026. The Fed’s June dot plot points to 3.8% by year-end, above today’s 3.625% midpoint, so the earliest realistic cuts look more likely in H1 2027 if inflation eases toward 2.5% to 3.0%.

- UK Interest Rate Forecast: UK interest rates could go down, but not soon. With the Bank Rate at 3.75%, services inflation at 3.7%, and the latest shift in the inflation backdrop, most forecasters now expect holds through the summer and see only a small cut in late 2026 if conditions improve.

- ECB Rates Forecast: ECB rates are more likely to stay on hold than fall soon. The ECB recently raised rates to 2.25%, and most expectations now point to any further action being another hike before cuts become a 2027 story.

- Canada Interest Rate Forecast: Canada’s interest rates are the most likely among the major economies to go down next. Weak GDP growth and trade-war pressure are building a case for cuts, but the most likely timing still looks like early 2027 rather than immediately.

- Australia Interest Rate Forecast: Australia’s interest rates could go down, but the RBA is still in wait-and-see mode. After holding at 4.35%, most economists expect current settings to last into 2027, with only a possible cut in May 2027.

- Japan Interest Rate Forecast: Japan’s interest rates are the outlier because they are still moving up, not down. After the June hike to 1.00%, the Bank of Japan remains on a gradual normalisation path toward a higher neutral rate.

These diverging paths across major central banks create opportunities to position yourself for the next interest-rate cycle. With NAGA, you can gain exposure through trading bonds, investing in stocks and ETFs, or by following and copying lead traders who specialise in macro and rate-driven strategies.

Global Interest Rate Policy — What Is Driving Every Central Bank in 2026

Before diving into each central bank individually, it is worth understanding the single macro event that is driving virtually every policy decision in 2026: the Strait of Hormuz conflict, which began in late February 2026 following an escalation between US-aligned forces and Iran-backed groups in the Persian Gulf. The conflict disrupted approximately 21% of global seaborne oil trade, pushing Brent crude above $125 per barrel — roughly $40 above pre-conflict levels. The knock-on effects have been severe and broadly transmitted, with CPI reaching the highest level since April 2023 in the US, and inflation remaining above the central bank’s target in most major economies.

The structural challenge for central banks is that this inflation is primarily supply-driven (an energy price shock), not demand-driven. Rate hikes cannot increase oil supply or reopen the Strait. However, central banks' credibility rests on demonstrating that they will not allow energy price shocks to embed into underlying (non-energy) inflation through wage spirals and second-round effects. That imperative — protecting inflation expectations, not solving the underlying supply problem — is what pushed the ECB to hike in June and what is keeping every other central bank in a hawkish or neutral posture even as their domestic economies slow.

The coordinated rate-cutting that ran from mid-2024 through early 2025 has reversed. The ECB hiked on June 11 (first since 2023), the BoJ hiked on June 16 (to 1%, highest since 1995), and the Fed's dot plot flipped from a projected cut to a projected hike. This is not a temporary pause — it is a policy regime shift driven by the Hormuz conflict.

US Interest Rate Forecast 2026

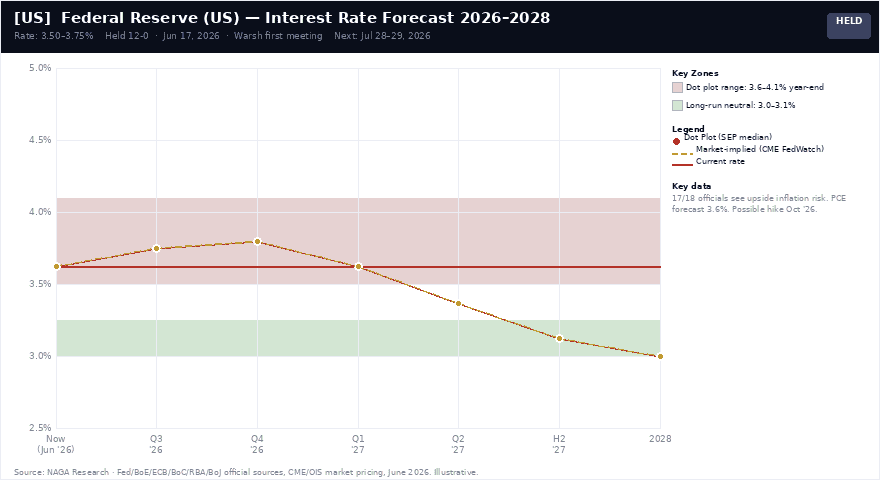

Kevin Warsh's first FOMC meeting as Fed chairman ended June 17 with rates unchanged at 3.50–3.75%, the level held since December 2025. Despite three cuts in late 2025, the outlook turned hawkish: the median projection for end-2026 rose to 3.8% from 3.4% in March, flipping from a cut signal to above today's 3.625% midpoint.

Nearly all participants (17 of 18) judged inflation risks as upside-weighted, with none seeing downside risk. Warsh shortened the statement to 130 words, removed easing-bias language, and the Fed lifted its 2026 PCE forecast to 3.6% due to the Middle East energy shock. Most officials now expect the benchmark to end 2026 between 3.6% and 4.1%, up from the prior 3.25%–3.75% range.

When Will US Interest Rates Go Down?

US interest rates are unlikely to go down in 2026. The Federal Reserve held at 3.50–3.75% on June 17, but its dot plot now shows a median year-end projection of 3.8% — implying a rate hike rather than a cut before December. Markets price approximately one 25bp hike by October 2026. The earliest realistic scenario for rate cuts is H1 2027, and only if US inflation returns sustainably toward 2.5–3.0%.

Next FOMC Meeting: July 28–29, 2026 US Dollar Index Live Chart →

US Interest Rate Forecast — Next 5 Years

The Fed's longer-run "neutral" rate — where rates neither stimulate nor restrict the economy — is now projected at 3.0–3.1% by the median FOMC participant, confirming that the era of near-zero rates is over. While officials still expect rates to drift down slightly in 2027 and 2028, they are predicting a much slower, more cautious descent. The implied path based on current projections: one potential hike in H2 2026 (to 3.75–4.00%), then gradual cuts through 2027 toward 3.0–3.25% as inflation returns toward target.

The pace of those cuts depends entirely on whether the Hormuz conflict resolves (allowing oil prices to fall) or becomes sustained (keeping energy inflation elevated and the Fed on hold). A ceasefire would accelerate the path toward cuts; a prolonged conflict delays them further.

UK Interest Rate Forecast 2026

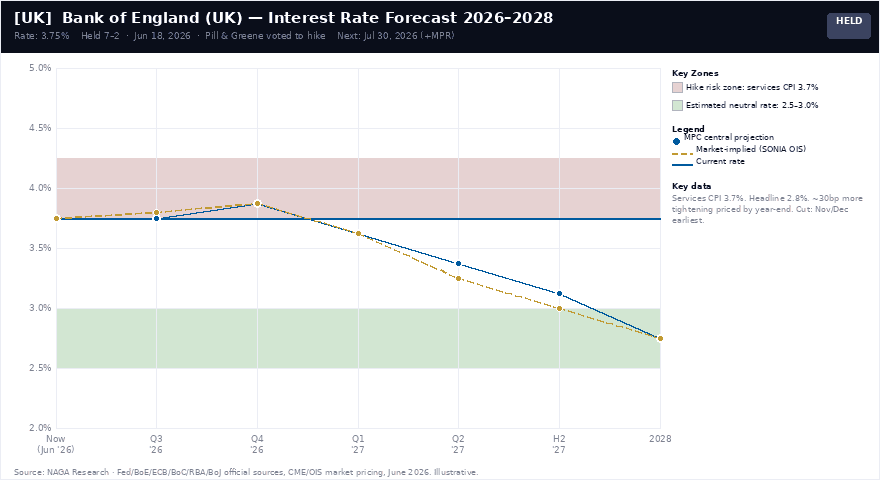

At its meeting ending on 17 June 2026, the Monetary Policy Committee voted by a majority of 7–2 to maintain the Bank Rate at 3.75%. Two members voted to increase the Bank Rate by 0.25 percentage points, to 4%. The BoE's statement acknowledged that energy prices had fallen since the previous meeting but remained above pre-conflict levels and volatile. UK CPI held at 2.8% in May — unchanged from April and below forecasts — but services inflation rose to 3.7%, the level that keeps the MPC hawkish even as headline inflation falls.

The base case for 30 July is a hold at 3.75% with a hawkish tilt while services inflation stays elevated, and a realistic chance of further dissents for a hike. Economists' 2026 forecasts span roughly 3.50% to 4.25%.

When Will UK Interest Rates Go Down?

UK interest rates are unlikely to fall in 2026. The Bank of England held at 3.75% on June 18 in a 7–2 vote, with two MPC members (including Chief Economist Huw Pill) already voting to hike to 4.00%. With UK services inflation at 3.7% — persistently above target — and the July 30 meeting carrying a new Monetary Policy Report, the most likely outcome is a series of holds through summer. Markets price roughly 30bp of additional BoE tightening by year-end, with a hike at the September or November meeting a realistic possibility rather than a tail risk.

UK Interest Rate Forecast — Next 5 Years

The Bank of England cut rates four times in 2025 from 5.25% to 4.25%, then once more to 3.75% in December 2025 — a total reduction of 150bp. The current hold reflects a mid-cycle pause rather than a pivot to tightening, though the two hawkish dissents complicate that narrative. The multi-year base case is broadly similar to the Fed: rates remain elevated in 2026, with gradual cuts beginning in 2027 toward a neutral rate of approximately 2.5–3.0%.

The key UK-specific variables are services inflation (the MPC's primary concern), wage growth (structurally elevated above 5% for three years), and the fiscal outlook under the new Labour leadership following Starmer's resignation — a political variable with potential gilt market implications that most interest rate models have not fully priced.

Pound forecast and price predictions

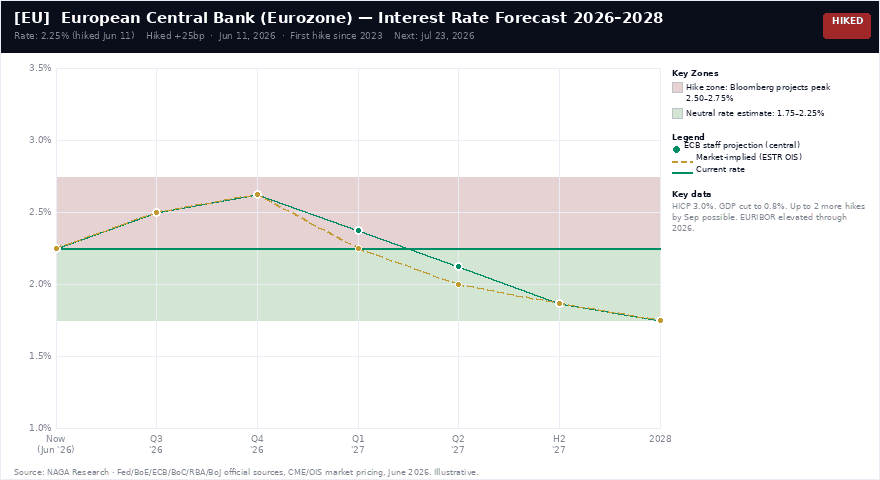

ECB Interest Rate Forecast 2026

At its 11 June 2026 meeting, the ECB raised its main interest rates by 0.25 of a percentage point, with the deposit rate raised to 2.25%. The ECB said rates were increased due to the conflict in the Middle East generating inflation pressures in the Eurozone. The ECB cut rates eight times from June 2024 to June 2025, before leaving rates unchanged until June 2026.

The ECB's June projections raised its 2026 inflation forecast to 3.0% (from 2.6%) while simultaneously cutting the 2026 GDP growth forecast to approximately 0.8%. This stagflationary combination — rising inflation in a weakening economy — is precisely the supply-shock dilemma that limits the ECB's ability to use rate cuts to stimulate growth without further fanning inflation. The next ECB meeting is July 23, when markets will watch for any signal of a second consecutive hike.

When Will ECB Rates Go Down?

ECB rates are not expected to go down in 2026 — they may go up further. The ECB raised its deposit rate to 2.25% on June 11, reversing the easing cycle that had run through 2024–2025. Bloomberg economists projected up to two additional hikes by September 2026, with the potential to reach 2.50–2.75%. ECB rate cuts are not expected until 2027 in the base case, and only if energy price pressures from the Hormuz conflict subside sufficiently. For markets tracking EURIBOR, this means the 3-month EURIBOR floor has moved materially higher, with implications for EUR mortgage and corporate borrowing rates.

ECB Forecast — Next 5 Years and EURIBOR Implications

The ECB's longer-term neutral rate — the rate it is trying to converge toward — is estimated at approximately 2.0–2.5%. The June hike to 2.25% means the ECB is near, or slightly above, neutral territory in its own estimation. Future hikes would explicitly constitute tightening into a slowing economy, a politically and institutionally difficult position given the fragility of sovereign debt in high-deficit member states like Italy (138.6% debt-to-GDP) and France.

A soft ceasefire resolution would allow energy prices to fall, potentially unlocking ECB cuts in H1 2027 toward 1.75–2.0%. For EURIBOR — the benchmark used in European mortgage and corporate lending rates — the June hike and any follow-on moves would keep EURIBOR at elevated levels through 2026, with downward movement only expected in 2027.

Euro to US Dollar forecast and price predictions 2026

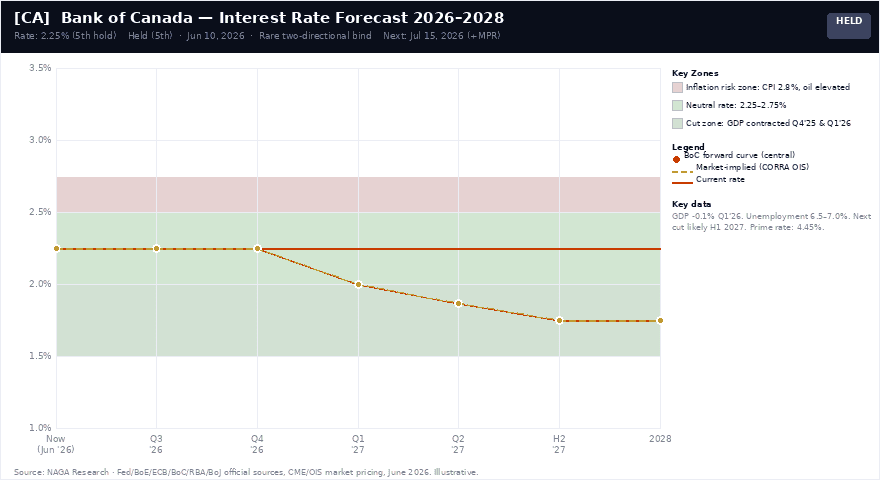

Bank of Canada Interest Rate Forecast 2026

The Bank of Canada held its key interest rate at 2.25 per cent on June 10, as the bank seeks to balance economic turbulence while keeping inflation from rising too much. Governor Tiff Macklem described the central bank's challenge explicitly: "Economic activity in Canada has been weak and uncertainty about US trade policy persists. The conflict in the Middle East is ongoing, and oil prices remain elevated.

Governing Council is continuing to look through the war's near-term impact on headline inflation, but will not let higher energy prices become persistent inflation." The BoC is unique among this group in facing a genuine two-sided bind: an economy weakened by US tariff headwinds (exports falling, business investment soft, GDP contracting) on one side, and an inflation risk from energy prices on the other. The hold reflects a rare two-directional bind.

When Will Canadian Interest Rates Go Down?

Canadian interest rates are not expected to fall materially in 2026. The Bank of Canada held at 2.25% on June 10 for the fifth consecutive meeting, caught between a softening economy (GDP declined in Q4 2025 and Q1 2026, unemployment 6.5–7.0%) and renewed inflation from energy prices (CPI at 2.8% in April). BMO expects holds through year-end. NAB has signalled the next move is more likely down, but timing is uncertain. Cuts are more likely in H1 2027 as the energy-driven inflation impulse fades.

Canadian Interest Rates — Next 5 Years

The Bank of Canada's projected rate path is the most dovish among this group of central banks. Having already cut from 5.0% to 2.25% between mid-2024 and early 2026 — one of the most aggressive easing cycles in Canadian monetary history — the BoC is at or near neutral rates (estimated at 2.25–2.75% for Canada).

Forward pricing and the BoC's own communications suggest broadly stable rates through 2026, with the next meaningful move being a cut in early 2027 as US trade policy clarity improves, the Hormuz inflation shock passes, and Canada's domestic economy recovers from the tariff headwinds. The prime rate (currently 4.45%) would follow any BoC cut, directly impacting Canadian variable-rate mortgage holders.

Oil forecast and price predictions 2026

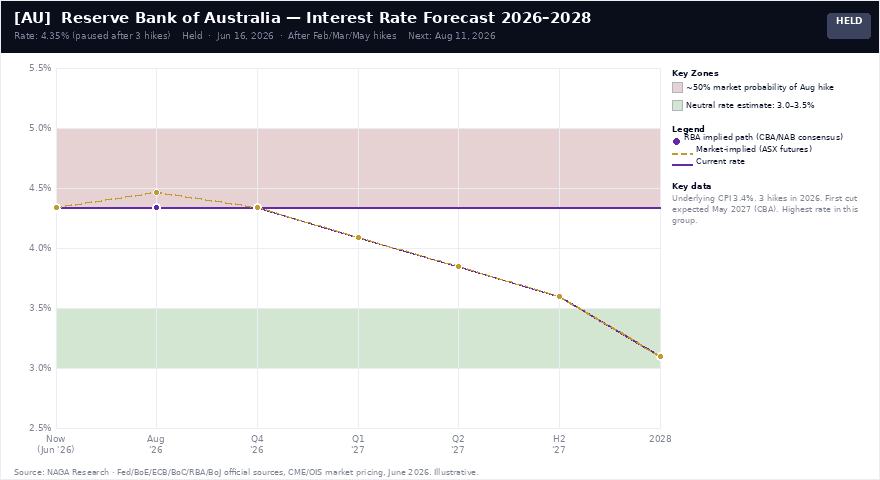

RBA Interest Rate Forecast 2026 (Australia)

The Reserve Bank of Australia has left interest rates on hold for the first time in 2026, pausing after three consecutive hikes as it weighs slowing growth, high inflation and the impact of oil supply disruption. The RBA left the cash rate unchanged at 4.35 per cent. The decision was unanimous. At its June meeting, the Board decided to leave the cash rate target unchanged at 4.35 per cent.

Inflation picked up materially in the second half of 2025, and information since the beginning of this year confirms that some of the increase reflected greater capacity pressures. The latest data show that headline and underlying inflation are still too high. Underlying inflation ticked up to 3.4% — above the 2–3% target — confirming that Australia's inflation challenge predated the Hormuz conflict and has been further complicated by it.

When Will Australian Interest Rates Go Down?

Australian interest rates are unlikely to fall in 2026. The Reserve Bank of Australia held at 4.35% on June 16 after three straight hikes in 2026 (February, March, and May). CBA economists expect the current rate to hold into 2027, with a possible first cut in May 2027 if inflation returns sustainably within the 2–3% target band. Markets price approximately a 50% chance of one further hike at the August 11 meeting. NAB has revised away from a further hike forecast but does not see cuts in 2026 either.

Australian Interest Rates — Next 5 Years

Australia's rate cycle has been more severe than most peers: the RBA hiked from 0.10% in May 2022 to 4.35% in mid-2026 — a total of 425bp — in a cycle driven by genuine domestic capacity pressures alongside global inflation. The RBA's longer-run neutral rate is estimated at approximately 3.0–3.5%. A path from 4.35% back to neutral implies 85–135bp of cuts over 2–3 years once inflation is sustainably within target.

CBA's forecast of a May 2027 first cut implies roughly 75–100bp of easing through 2027–2028, with rates potentially reaching 3.35% by end-2027. That path is contingent on the Hormuz conflict resolving (reducing energy costs) and Australian wage growth moderating from its current elevated pace.

Gold forecast and price predictions 2026

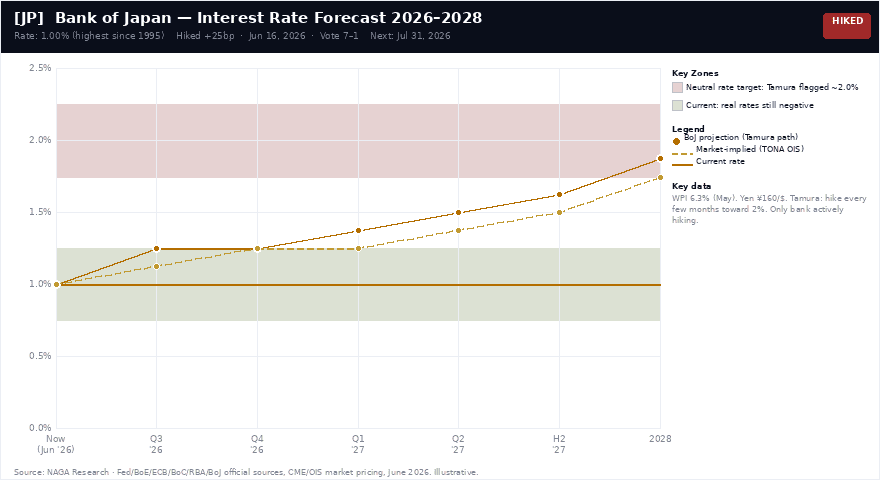

Bank of Japan Interest Rate Forecast 2026

As expected, Japan's central bank raised its policy rate to the highest in over 30 years at 1%, accelerating policy normalisation started in 2024. The decision was split 7-1, with board member Toichiro Asada dissenting and advocating for a hold. The BoJ cited Japan's wholesale inflation of 6.3% in May — the highest since March 2023 — and a yen that had weakened to 160 against the dollar despite intervention operations of 11.7 trillion yen in May.

A weak yen, despite boosting the competitiveness of Japan's exports, will increase imported inflation and pressure government finances as it seeks to cushion the impact of rising prices via subsidies. BoJ Deputy Governor Himino reinforced the hawkish message on June 24, stating the BoJ would "continue raising interest rates while closely monitoring the risk that underlying inflation could exceed its 2% target."

When Will Japanese Interest Rates Go Down?

Japanese interest rates are not going down — they are going up. The Bank of Japan hiked to 1.00% on June 16, its highest rate since 1995, and board member Tamura explicitly flagged a neutral rate of approximately 2.0% as the target, with hikes "at intervals of a few months." Japan is the only major central bank still in a firm tightening cycle in mid-2026. Rates are expected to continue rising toward 1.25–1.50% by end-2026 and possibly 1.75–2.00% by 2028.

Japan Interest Rates — Next 5 Years

Japan's normalisation from ultra-loose monetary policy is the most structurally significant monetary policy development in the global economy over the next five years, with implications far beyond Japan's borders. The BoJ's gradual rate rise — from -0.10% in early 2024 to 1.0% today, with a target of approximately 2.0% by 2028 — is progressively unwinding the yen carry trade that has kept global asset prices elevated and the yen weak.

Each additional BoJ hike narrows the yen's yield differential against the dollar, euro, and pound, supporting yen appreciation and putting mild downward pressure on global risk assets. Board member Tamura's explicit "neutral rate of around 2%" target implies four to five more 25bp hikes through 2026–2028, with rates reaching approximately 1.75–2.00% by 2028. This path is conditional on Japan's underlying inflation remaining at or above 2% — the first time in decades that condition has been met sustainably.

How to invest in the Japanese stock market

Interest Rates Forecast Summary — All Major Central Banks

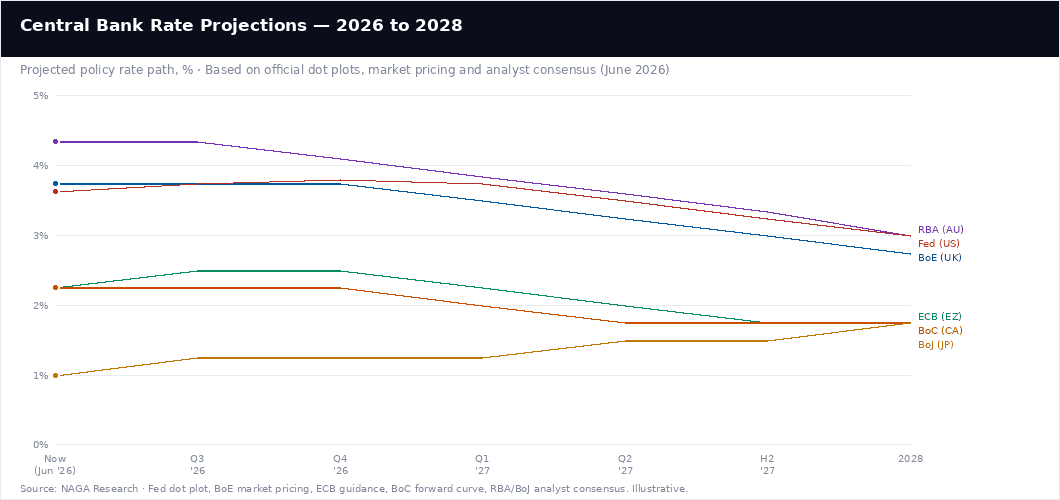

Central Bank Current Rate Last Decision Next Meeting H2 2026 Outlook 2027 Forecast Direction Fed (US) 3.50–3.75% Held, Jun 17 Jul 28–29 Possible hike to 3.75–4.00%; median dot plot 3.8% year-end Gradual cuts toward 3.0–3.25% ▲ Hike risk BoE (UK) 3.75% Held 7–2, Jun 18 Jul 30 (+ MPR) Hold likely; one hike to 4.00% possible at Sep/Nov if services inflation stays >3.5% Cuts toward 2.75–3.00% ■ Hold / Hike risk ECB (Eurozone) 2.25% Hiked +25bp, Jun 11 Jul 23 Possible second hike to 2.50%; Bloomberg projects peak of 2.50–2.75% by Sep Cuts toward 1.75–2.00% ▲ Hiking BoC (Canada) 2.25% Held (5th), Jun 10 Jul 15 (+ MPR) Hold through year-end; bias tilting toward eventual cut Cuts toward 1.75%; easing begins H1 2027 ■ Hold RBA (Australia) 4.35% Held, Jun 16 (after 3 hikes) Aug 11 Hold likely; ~50% market probability of one more hike in Aug Cuts begin ~May 2027 toward 3.35% ■ Hold / Hike risk BoJ (Japan) 1.00% Hiked +25bp, Jun 16 Jul 31 Hikes continue at "intervals of a few months"; target ~1.25–1.50% by year-end Further hikes toward 1.75–2.00% neutral rate ▲

Interest rate forecasts are based on current economic data, official central bank communications, and market pricing as of June 26, 2026. Forecasts are subject to change and do not constitute investment or financial advice. Past performance is not a reliable indicator of future outcomes. The interest rate paths shown are illustrative central tendencies, not guaranteed outcomes.

Will Interest Rates Go Down in 2026?

For most of the world's major economies, no — not meaningfully in 2026. The Strait of Hormuz conflict has fundamentally altered the interest rate outlook for 2026 across all major economies. What was, at the start of the year, widely expected to be a year of coordinated rate cuts has become a year of holds, hesitations instead, and in some cases additional hikes. Here is how each central bank stands on the key question:

Federal Reserve - Not in 2026

Base case: one hike by October 2026

Median dot plot projects 3.8% year-end. Earliest cuts: H1 2027. Requires CPI to fall toward 2.5–3.0%.Bank of England - Unlikely in 2026

Base case: hold; hike at Sep/Nov/Dec possible

Services inflation at 3.7% blocks cuts. Small chance of 25bp cut at Nov or Dec if inflation surprises lower.ECB - Inverted, hiking

Up to 2 more hikes possible; peak 2.50–2.75%

Rates went UP in June 2026. Cuts expected from early 2027, contingent on energy price resolution.Bank of Canada - Not in 2026

Hold through year-end; cuts begin H1 2027

Most likely to cut next among this group, but not until 2027. Economy weak; inflation still elevated.RBA (Australia) - Possibly hiking

50% market probability of one more hike (Aug)

First cut expected May 2027. Three hikes already delivered in 2026; highest rate of the group at 4.35%Bank of Japan - Hiking

Targeting ~1.25–1.50% by year-end 2026

Explicitly tightening. Target neutral rate of 2.0% by 2028. Rates will not go down in Japan for years.

The most important caveat: all of these forecasts are conditional on the Hormuz conflict and energy prices. A durable US-Iran ceasefire — including a confirmed reopening of the Strait and sustained falls in Brent crude toward $90–$95 — would meaningfully change the calculus for the Fed, ECB, and BoE within one to two inflation print cycles (roughly three to four months). In that scenario, rate cuts could arrive sooner than the base cases above — perhaps as early as Q4 2026 for the most dovish central banks. Conversely, an escalation that pushes oil above $140–$150 sustained would delay cuts further and increase the probability of additional hikes across all jurisdictions simultaneously.

Learn to Trade Interest Rate Moves with NAGA

- Practice trading interest rate-sensitive assets — bonds, forex, indices — with $100,000 in virtual funds. No risk, real markets.

- Learn how interest rate decisions affect forex (GBP/USD, EUR/USD), bond yields, and equity markets in our free educational hub.

Disclaimer: The information provided is for general informational purposes only and does not constitute investment advice, an investment recommendation, a personalised recommendation, or an offer or solicitation to engage in any investment activity.

Sources

- Federal Reserve — FOMC Statement, June 17, 2026

- Federal Reserve — FOMC Meeting Calendars

- Bank of England — Monetary Policy Summary and Minutes, June 2026

- European Central Bank — Governing Council monetary policy decisions, June 11, 2026 (via House of Commons Library citation of ECB)

- Bank of Canada — Press Release, Interest Rate Announcement, June 10, 2026

- Bank of Canada — Monetary Policy Report, April 29, 2026

- Reserve Bank of Australia — Statement by the Monetary Policy Board, June 2026

- Bank of Japan — Statement on Monetary Policy, June 16, 2026 (PDF)