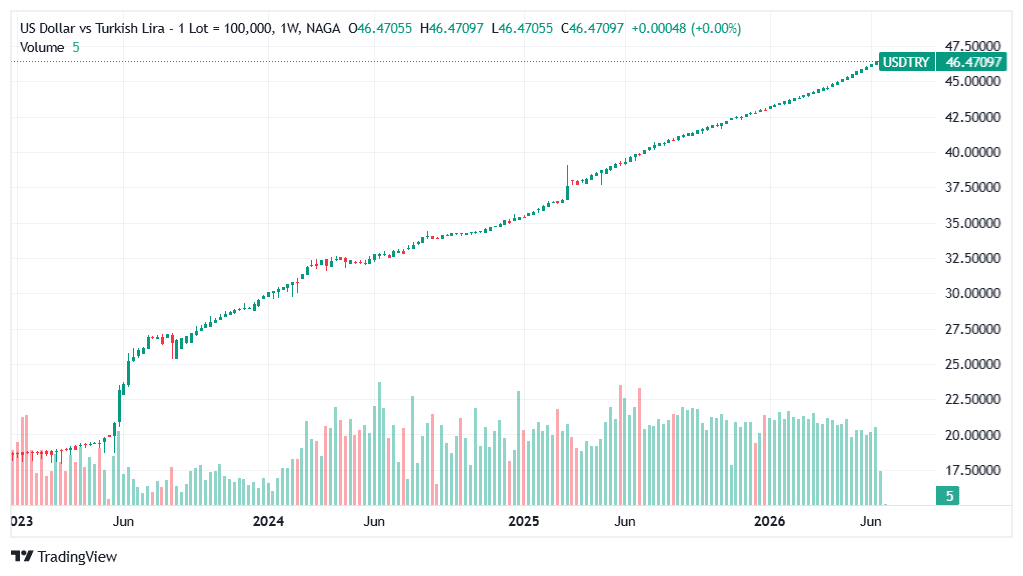

The Turkish lira's trajectory in 2026 can be summarised in two words: managed, predictable. Since Finance Minister Mehmet Şimşek assumed office in mid-2023 and shifted Turkey's economic policy framework toward orthodox monetary management, USD/TRY has followed a remarkably steady depreciation gradient — approximately 7–9 lira per year — rather than the violent, disorderly crashes that characterised the pre-2023 era.

The lira is down about 8% year-to-date against the dollar and roughly 17% over the past 12 months, tracking very close to the inflation differential between Turkey (32.6% CPI) and the US (4.2% CPI). This is precisely what the TCMB's disinflation framework intends: a controlled, nominal depreciation that avoids outpacing monthly inflation, thereby preventing currency weakness from feeding back into inflation expectations and derailing the disinflation path.

The risk to this orderly picture comes from two directions. First, the Strait of Hormuz conflict has driven energy prices sharply higher, and Turkey — as a major oil and gas importer — is particularly exposed. Inflation re-accelerated, and the TCMB has responded by pausing its easing cycle and tightening effective liquidity conditions. Second, political uncertainty flared in early 2025, demonstrating that Turkish politics can still trigger sharp lira selloffs that disrupt the TCMB's orderly management plan.

Turkish Lira Forecast & Price Prediction 2026 – Summary

- Turkish Lira forecast H2 2026 — USD/TRY: The managed depreciation path implies roughly 1–2% per month of additional lira weakness, clustering between 49 and 51.4 for year-end 2026:

- BASE CASE ~60% (USD/TRY 48 – 51): Managed depreciation continues at ~1 –2% monthly pace, consistent with the post-Şimşek framework. TCMB holds at 37 %, inflation stabilises in the 27–33% range, political situation normalises. Lira weakens predictably and slowly — consistent with all major model projections.

- BEAR CASE (Lira) ~25% (USD/TRY 53 – 60+): A political shock — election surprise, Şimşek departure, or a court ruling perceived as undermining the TCMB's independence — combined with sustained high energy prices triggers a carry-trade unwind. USD/TRY breaks above 50 decisively and accelerates toward 55–60 as foreign investors exit Turkish lira-denominated assets rapidly. Similar to the January 2025 İmamoğlu episode but more sustained.

- BULL CASE (Lira) ~15% (USD/TRY 42 – 46): The Iran ceasefire holds definitively, and oil falls sharply, easing Turkish energy import costs and allowing inflation to resume its disinflation path faster than expected. The TCMB resumes cutting rates — reducing the forward depreciation premium — while strong tourism revenues ($100B+ again) support the current account. USD/TRY stabilises or modestly reverses toward 42–44.

- Turkish Lira price prediction 2027: The outlook depends almost entirely on whether Turkey's disinflation program returns to track after the 2026 energy-shock interruption. In the base case — oil prices moderate in H2 2026 after ceasefire implementation, allowing the TCMB to resume gradual rate cuts and inflation to resume falling toward 20% or below by end-2026 — USD/TRY would likely continue its managed depreciation but at a slower pace, reaching approximately 50–54 by end-2027

- Turkish Lira forecast 2030: The structural case for continuing lira weakness through 2030 is compelling — if Turkey's inflation structurally exceeds that of its trading partners, purchasing power parity theory implies ongoing nominal depreciation. However, if Şimşek's framework succeeds in bringing inflation toward the TCMB's 5% medium-term target by 2028–29 — USD/TRY would still weaken from today but at a much slower pace, perhaps reaching 55–65 by 2030 rather than 80–90.

Trade Turkish Lira with NAGA: You can trade CFDs on USD/TRY and EUR/TRY with low fees, tight spreads, and an easy-to-use interface.

High-interest-rate currencies like the Turkish lira are very attractive to those who are aiming for swap points in forex trading. However, for beginners, trading for Turkish lira swap points carries a great deal of risk.

Follow the USD/TRY, EUR/TRY, and GBP/TRY price charts for live data, and read our latest Turkish Lira forecast and price predictions for 2026 and beyond. Key pivot points and support and resistance levels provide further insights to help you make informed trading decisions.

Turkish Lira Fundamental Analysis 2026

Understanding the Turkish lira's behaviour requires accepting that it operates in a genuinely unusual macro regime — simultaneously one of the world's highest nominal interest rates (37–40%), one of the highest inflation rates among G20 economies (32.6%), and one of the most actively managed exchange rate paths in the emerging markets.

The TCMB's Disinflation Framework — Where It Stands

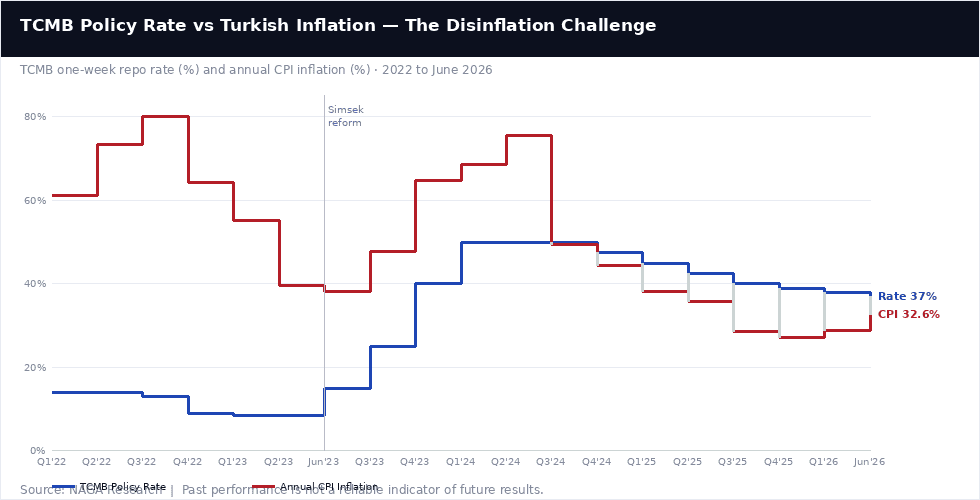

The Central Bank of the Republic of Turkey (TCMB) under Governor Fatih Karahan has maintained a strictly orthodox policy framework since inheriting the role from Hafize Gaye Erkan in 2024. The policy rate trajectory tells the story: from a pre-Şimşek era where rates were cut to 8.5% even as inflation ran above 80%, to an aggressive hiking cycle that took the one-week repo rate to 50% by Q1 2024, followed by cautious, data-dependent cuts back toward 37% by early 2026. That easing cycle was then paused — three consecutive holds since March 2026 — as the Iran conflict drove energy prices sharply higher and re-accelerated inflation.

The TCMB has been explicit about its reaction function: rate cuts will only resume when monthly inflation prints are consistent with a return to the disinflation path, and any sign of currency instability will be met with both rate holds and foreign exchange intervention. The bank has already demonstrated the latter — it intervened in FX markets during the January 2025 İmamoğlu shock and suspended one-week repo auctions (effectively lending at the 40% overnight rate) as the Iran conflict began in early 2026. The result is a pair of tools working in the same direction: tight monetary policy defending the lira against inflation expectations, and active management defending it against acute market stress.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

The chart above illustrates the most important development in Turkish monetary policy in a decade: for the first time since the 1990s, Turkey has a policy rate that meaningfully exceeds inflation — real positive interest rates, however modest. The TCMB rate at 37% versus inflation at 32.6% implies a real rate of approximately 4.4% — narrow, but positive, and a complete reversal from the deeply negative real rates that characterised the 2021–2022 period when inflation ran at 60–80% while rates were held at 8–14%.

This real-rate framework is the foundation of the Şimşek disinflation strategy, and its durability is the single biggest determinant of the lira's managed depreciation continuing at its current orderly pace versus reverting to chaotic collapse.

Inflation — The Interrupted Disinflation

Turkey's inflation story in 2025–2026 was meant to be one of the most dramatic disinflationary journeys in emerging markets: from 75.5% in May 2024 to a projected 13–19% by end-2026 under the TCMB's own forecast. Progress was real and significant — CPI fell to 27.1% by December 2025, a drop of nearly 50 percentage points from the peak in under 18 months.

Then the Strait of Hormuz conflict intervened. Turkey imports approximately 90% of its oil and gas needs, making it structurally one of the most energy-inflation-exposed economies in the G20. Monthly CPI rose 4.18% in April and 1.7% in May 2026, taking annual CPI back to 32.6% — with the TCMB updating its end-2026 inflation forecast to 26% (from a range of 15–21% previously). The disinflation has not been abandoned, but it has been interrupted — and whether oil prices moderate in H2 2026 (a ceasefire resolution) or remain elevated is the single biggest near-term determinant of whether the original 15–21% year-end target is achievable.

Current Account and Reserves

Turkey's current account deficit has narrowed significantly under the Şimşek framework, supported by record tourism revenues (on track for $100B+ in 2026), strong export performance, and tighter domestic demand suppressing import growth. Gross foreign exchange reserves stand at approximately $54.2 billion (as of May 22, 2026), a meaningful improvement from the negative net-reserve position in 2021.

These reserves provide the TCMB with genuine firepower for FX interventions, and their restoration under the current policy framework has been one of the most important signals of improved institutional credibility. The key vulnerability remains energy import dependency: with oil prices elevated due to the Hormuz conflict, the current account will remain under pressure even as tourism inflows rise.

Political Risk — The Persistent Overhang

No analysis of the Turkish lira is complete without acknowledging political risk. The January 2025 arrest of Istanbul Mayor Ekrem İmamoğlu — a major opposition figure widely seen as a potential presidential rival to Erdoğan — triggered a brief but sharp USD/TRY spike to approximately 41.2, requiring direct TCMB intervention. The bank's June 2026 statement itself referenced a recent court ruling affecting opposition leader Özel as a factor that tested lira stability.

Finance Minister Şimşek's continued presence in government is widely regarded as essential to market confidence — his departure or a perceived policy reversal would likely trigger a severe lira selloff. This political sensitivity creates asymmetric risk: the base case is orderly managed depreciation, but tail events driven by domestic politics can be violent and fast.

Turkish Lira (TRY) Technical Analysis

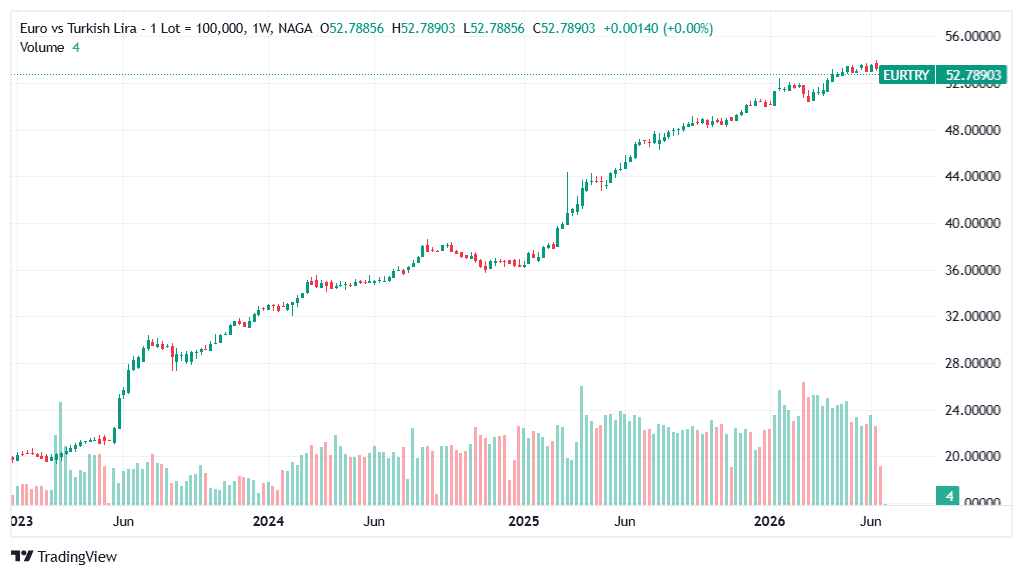

The technical picture for TRY is unusual in one key respect: every level is uncharted territory. The US Dollar and Euro have set a new all-time high every single month since the Şimşek reform era began in mid-2023, broken only by the brief post-İmamoğlu consolidation in Q2–Q3 2025. There is no technical resistance — only the slope and pace of the uptrend, and the psychological round-number levels.

For both USD/TRY and EUR/TRY, the dominant visual pattern is a near-perfectly linear ascending trend with one clear interruption: the January 2025 İmamoğlu spike, which briefly overshot the trend before quickly reverting. This is the textbook's signature of managed depreciation — the TCMB is effectively acting as a trend-enforcer, intervening when the pace deviates too far in either direction.

The absence of any technical consolidation chart patterns (triangles, ranges, channels) is itself informative: these pairs do not consolidate; they just rise at a controlled pace.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

Read also: Euro to Dollar Forecast & Price Predictions 2026

Turkish Lira Forecast 2026 — Institution Predictions

Major financial institutions and rating agencies have issued updated forecasts for the Lira’s performance against the U.S. Dollar (USD) in 2026, with most projecting continued weakness under prevailing macroeconomic conditions.

Institution USD/TRY Target Horizon Key Driver Goldman Sachs 48.0 July 2026 Further rate cuts and carry trade unwinding; still broadly on track versus current spot Morgan Stanley 44.0 Q4 2026 Stronger CEEMEA positioning in the earlier forecast; now best treated as a dated reference point JPMorgan 45.50 End-2025 Falling inflation if policy stays unchanged; useful as a prior anchor, but no fresh 2026 target is stated ING 51.0 End-2026 Controlled depreciation as inflation eases and policy rates trend lower S&P Global Ratings ~47.0 End-2026 Cautious outlook, with inflation still in the high teens and reform credibility still important Deutsche Bank 52.0 End-2026 Bearish medium-term view, including weaker carry-trade support Trading Economics 41.59 12 months from Sep 2025 Mild depreciation in global macro models; best used as a conservative short-horizon benchmark ExchangeRates.org.uk 50.71 Year-end 2026 Managed-depreciation path based on weighted averages of major sources

AI-Based Turkish Lira Forecasts

Algorithmic and AI-driven models for USD/TRY show unusual agreement: virtually all of them project continued lira weakening, differing only in pace. This is one of the few currency pairs where the algorithmic consensus and the fundamental/institutional view point in the same direction — because the managed depreciation trend is so persistent and consistent that even backwards-looking momentum models pick it up reliably.

Model End-2026 End-2027 2030 Notes CoinCodex ~51.37 Ongoing weakness N/A Most bearish 2026; range 46.24–51.37 for the year; algorithmic momentum model. LongForecast 49.86 ~52–53 ~88–90 Monthly mechanical model; consistent 1–2% monthly depreciation; projects ~88 by early 2030. WalletInvestor N/A (older data) N/A ~83 (2031) Long-term bullish on USD/TRY (bearish lira); +89.63% from ~43.75 over 5 years implied ~83 by 2031. TradersUnion ~50.22 ~47.17 ~59.92 Most conservative long-term model — projects a moderation in depreciation pace if disinflation resumes. Unique in showing a 2027 partial reversal before resuming higher. Panda Forecast AI ~48–49 N/A N/A Bullish on USD/TRY (bearish lira); broadly tracks Goldman Sachs 48-by-July thesis extended through year-end.

The TradersUnion model is particularly noteworthy for its 2027 projection: at 47.17, it suggests that if Turkey's disinflation resumes strongly in H2 2026–2027, the pace of nominal depreciation could actually slow enough for the 2027 average to be below the 2026 year-end level — implying a brief period of relative lira stability. This is the most optimistic algorithmic view and contrasts sharply with LongForecast's simple extrapolation toward 88–90 by 2030.

The wide range between these models — roughly 60 to 90 for USD/TRY by 2030 — illustrates why 5-year TRY forecasts should be treated as structural directional frameworks rather than actionable price targets.

AI and algorithmic forecasting models are based on historical data patterns and should not be used as the sole basis for trading decisions. Past performance and algorithmic projections are not reliable indicators of future results.

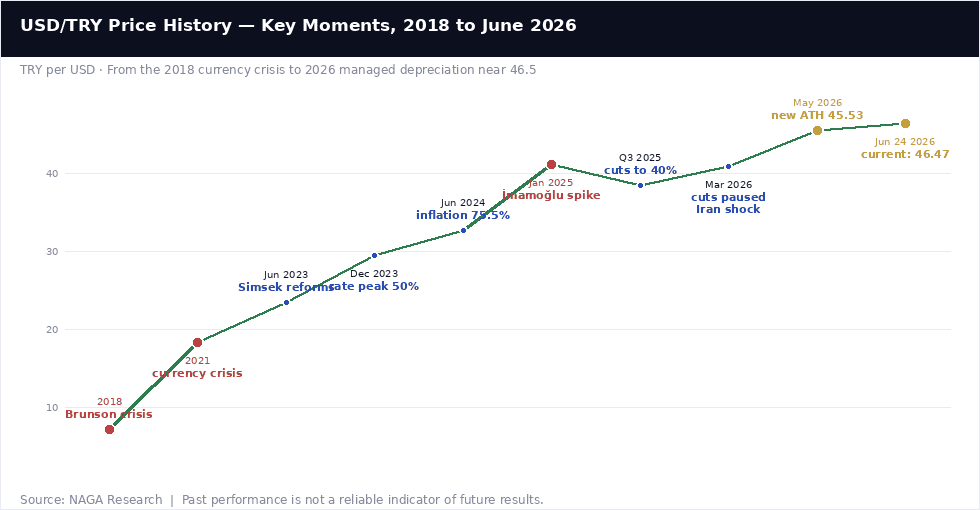

USD/TRY Price History — Key Moments

The Turkish lira's modern history is defined by a sequence of crises separated by brief recoveries — each recovery shorter and shallower than the last, with the 2023 Şimşek reform representing the most serious attempt since the early 2000s to break the cycle through orthodox monetary policy.

2018: The Brunson Crisis (USD/TRY ~7.24)

The Trump administration's imposition of tariffs and sanctions on Turkey in August 2018 — centred on the detention of American pastor Andrew Brunson — triggered the lira's first major modern crisis, with USD/TRY spiking to 7.24 at the height of the episode (a level that seems impossibly low from today's vantage point). The TCMB had been holding rates below inflation for political reasons, and the crisis exposed the structural fragility of this approach. The lira eventually recovered as Brunson was released and US sanctions eased, but the episode established the template for subsequent crises: political event → lira spike → TCMB crisis response → partial recovery.

December 2021: The Currency Crisis (USD/TRY ~18.36)

The most severe pre-Şimşek lira collapse occurred in December 2021, when President Erdoğan's insistence on cutting rates despite soaring inflation drove the lira to 18.36 per dollar — a loss of approximately 44% of its value in a single year. Erdoğan's unconventional "interest rates cause inflation" thesis led to a series of rate cuts even as CPI accelerated toward 80%, eventually triggering a near-hyperinflationary episode. The crisis was only partially contained through costly foreign exchange interventions and a novel lira-protected deposit scheme (KKM) that transferred exchange rate risk from depositors to the Turkish government.

June 2023: The Şimşek Reform Pivot

Erdoğan's re-election in May 2023 was followed by an unexpected policy reversal: the appointment of former Merrill Lynch banker Mehmet Şimşek as Finance Minister and Hafize Gaye Erkan (later replaced by Fatih Karahan) as TCMB Governor, with an explicit mandate to restore orthodox monetary policy. Interest rates were hiked aggressively from 8.5% to 50% by Q1 2024, the KKM scheme was wound down, and fiscal policy was tightened. USD/TRY, which had been at 23.50 when the reform began, continued to rise — but at a controlled, managed pace rather than chaotically. This distinction between "managed depreciation" and "crisis depreciation" is the central achievement of the Şimşek era.

January 2025: The İmamoğlu Spike

The arrest of Istanbul Mayor Ekrem İmamoğlu on March 19, 2025 (preceded by growing legal pressure in January) triggered a brief but sharp lira selloff, with USD/TRY spiking to approximately 41.2 before the TCMB intervened aggressively through direct FX market sales and suspension of one-week repo auctions. The episode was significant for two reasons: it demonstrated that political risk remains a live tail-risk even under the Şimşek framework, and it demonstrated that the TCMB was both willing and able to defend the lira's managed path when sharp deviations occurred.

2026: The Iran Shock and Inflation Re-acceleration

The Strait of Hormuz conflict, beginning in late 2025 / early 2026, derailed Turkey's disinflation path at a critical moment. With inflation having fallen to 27% by the end of 2025 — and the TCMB having cut rates from 50% to 38% in five moves — the energy price shock pushed CPI back to 32.6% by May 2026. The TCMB paused its easing cycle, suspended one-week repo operations to tighten effective rates to 40%, and the lira resumed its managed depreciation path while the energy shock played out. USD/TRY topped 45.53 intraday in May (a new all-time high) and currently trades at 46.47, down approximately 7% year-to-date — broadly on the managed path but with renewed uncertainty about when the next rate cut phase can begin.

*It is worth keeping in mind that both analysts and online forecasting sites can and do get their predictions wrong. Keep in mind that past performance and forecasts are not reliable indicators of future returns. When considering Turkish Lira price predictions for 2026 and beyond, it’s important to keep in mind that high market volatility and the macroeconomic environment make it difficult to produce accurate long-term Turkish Lira analyses and estimates. As such, analysts and forecasters can get their forecasts wrong.

It is essential to do your research and always remember that your decision to trade depends on your attitude to risk, your expertise in the market, the spread of your investment portfolio, and how comfortable you feel about losing money. You should never invest money that you cannot afford to lose.