The US Dollar again heads downhill and continues under pressure, particularly from European investors. The US Dollar Index lost 0.37% of its value during yesterday’s Asian and European trading session before correcting back upwards. This morning, the index again declined by 0.31% during the Asian session alone. The Dollar comes under pressure from potentially lower inflation and a softer stance by the Federal Reserve. However, the price of Gold saw little bullish price movement as investor sentiment significantly increased and turned mainly towards risk-based assets.

The higher risk appetite can largely be seen in the US stock market. The NASDAQ rose 1.76% during the day, the S&P 500 by 0.93%, and the Dow Jones by 0.56%. European equities, including the German DAX, FTSE100, and French CAC, also witnessed bullish price movement. However, the European Central Bank, like the Bank of England, is expected to continue hiking at the following two rate decisions. Investors should note that there is also an increased level of interest in the stock market, specifically in tech stocks, due to the stimulus in China.

The Central Bank of China has lowered its interest rates by 0.10% to 1.90% to support economic growth, and experts advise that the government is also likely to follow with fiscal stimulus. Economic growth improves company performance, profits, and dividend payments. As a result, the price of stocks can be supported, specifically tech stocks. For example, China made up 22% of its iPhone sales in 2022, higher than in 2021.

When looking at the currency market, today's best-performing currency is the British Pound. This is due to the latest employment data which the Office of National Statistics made public this morning. The Euro is also performing well this morning and is only declining against the Pound. However, the currency market is likely to see higher levels of volatility, and the price depends on this afternoon’s US inflation data.

GBP/USD - US Dollar Stumbles

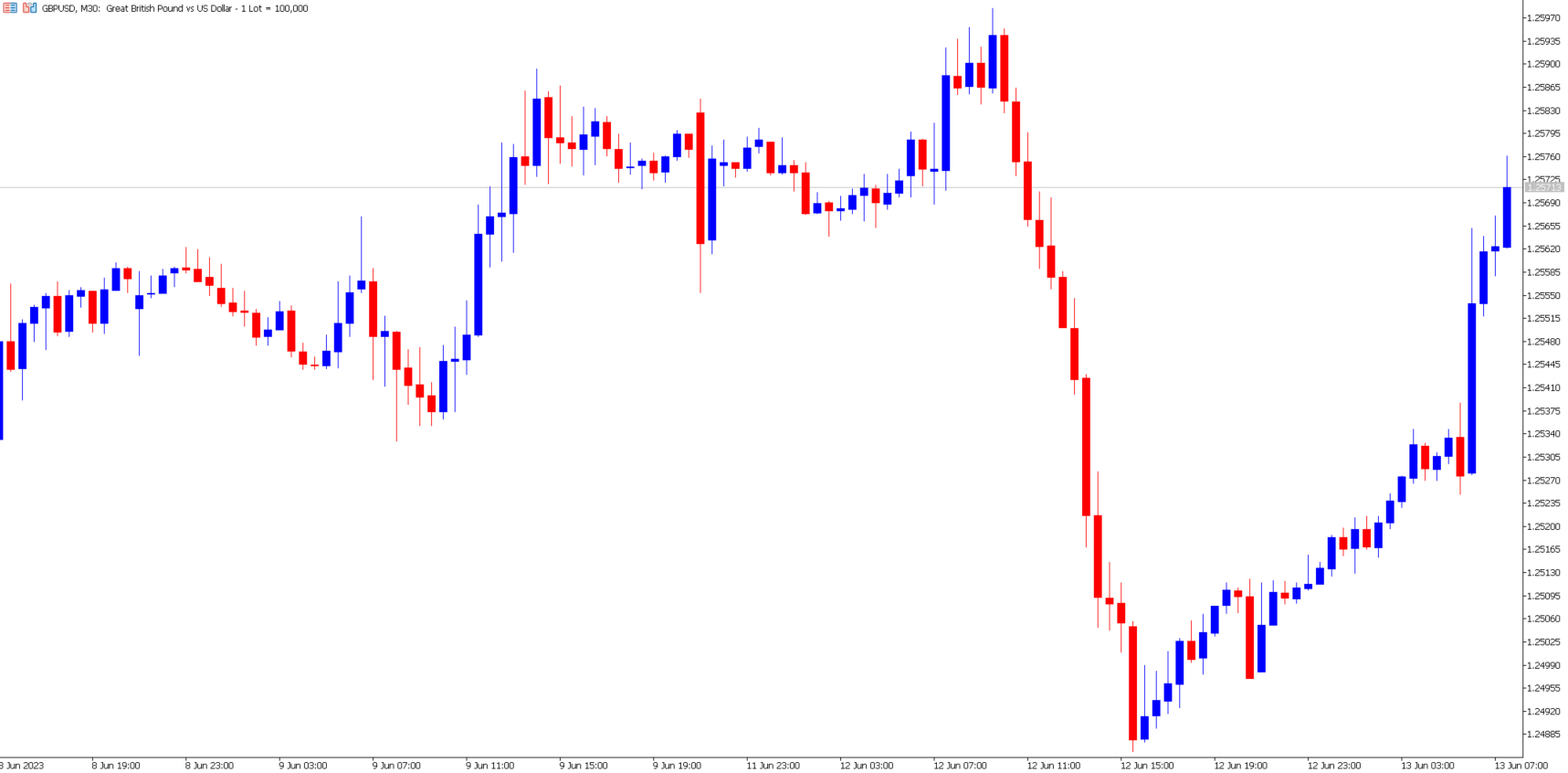

During today's trading, the GBP/USD declined for the first time in more than a week due to the Pound depreciating and less related to the Dollar. However, this morning the Pound is strongly supported by the UK’s latest employment data. As a result, the exchange rate is 0.40% higher, but has not yet corrected to previous highs. As mentioned above, the Dollar is also under pressure from the market's expectations related to inflation and monetary policy.

This morning, the UK released its latest employment data for May. The UK’s Claimant Count Change read -13,600, whereas markets initially expected 21,000 more unemployed jobseekers. In addition to this, the UK’s average salary continues to rise by 6.5%, much higher than the market’s 6.1% prediction. As a result, we can see the employment sector remains resilient, and demand remains high. Also, employees demand higher salaries to outweigh the cost of living crisis and debt. Consequently, the Bank of England is likely to continue hiking rates.

The market is more or less set on the Fed pausing after tomorrow’s Federal Open Market Committee meeting. However, the forward guidance given by the Fed will be essential, and economists are also contemplating whether the market will believe the forward guidance. For example, investors may not bite the bait if the chairman is slightly hawkish, which may be viewed as “uncertain” and “weak”.

The price action of the exchange rate is less certain than other pairs. The GBP/USD is forming lower lows on smaller timeframes but higher lows on larger timeframes. Nonetheless, the Bollinger Bands are currently pointed upwards, and the price is trading above the 150 Simple Moving Average. Lastly, Moving Averages have crossed over upwards. All the above are indications of a bullish trend. Nonetheless, this is likely to change if the price declines below 1.25200.

NASDAQ - Investor Venture To Riskier Assets

The price of the NASDAQ during yesterday’s trading experienced significantly higher levels of buy orders compared to sell orders. The index also saw its most significant price increase since May 26th. The NASDAQ has appreciated more than three times that of the SNP500 and continues to be supported by various economic and fiscal developments. Only Apple stocks declined in price from the top ten weighted stocks within the NASDAQ.

The latest price driver comes from the US and Chinese monetary policy. The US inflation rate is predicted to decline to 4.1%, which is lower than in recent months and is significantly closer to the Federal Reserve’s 2% target. Lower inflation results in higher consumer demand and a less hawkish central bank. Both are known to support the stock market, and investors should note that the NASDAQ is also partially correlated with the Chinese economy.

The NASDAQ has passed on the 61.8 mark on the Fibonacci Retracement levels. The next level on the Fibonacci, which may indicate a retracement, is at $16,553, but price action suggests the resistance level at $15,285. These are two levels that traders will continue monitoring. However, it should be noted the price will largely be influenced by today’s inflation data and tomorrow’s forward guidance.

Summary:

- The US Dollar Index lost 0.37% of its value during yesterday’s trading sessions before correcting upwards. However, the index is again declining this morning

- Investors expect US inflation to decline to 4.1% and the Fed to take a pause in the hiking cycle.

- The NASDAQ rose 1.76% during the day, the S&P 500 by 0.93%, and the Dow Jones by 0.56%.

- The UK’s Claimant Count Change read -13,600, whereas markets initially expected 21,000 more unemployed jobseekers. In addition to this, the UK’s average salary continues to rise by 6.5%, much higher than the market’s 6.1% prediction.