The DAX30 index opened the year on a historic note, crossing 25,000 points for the first time on January 7, building on 34 separate all-time highs notched in 2025 alone. The rally extended through the first quarter, with chart analysts at the Association of Technical Analysts of Germany flagging upside targets of 27,200 and even 28,800 — before US tariff threats against the EU in April triggered a sharp reversal that took the index back down toward 21,900, erasing the bulk of the year's gains in a matter of weeks.

Since that April low, the DAX has staged a steady recovery, helped by easing US–Iran tensions, an imminent US–Iran ceasefire agreement, and the European Central Bank's own policy moves. Despite negative German consumer sentiment, DAX constituents' global revenue exposure (the majority of large German companies earn most of their revenue outside Germany) has decoupled index performance from the struggling domestic economy.

DAX 30 Forecast 2026 — Summary

- DAX forecast H2 2026: From the 25,000 key resistance level, most banks see the DAX grinding higher into year-end, but the path depends heavily on whether the Iran ceasefire holds and how the ECB's new hiking bias evolves.

- BASE CASE (~50%) — 25,500 – 26,500: The ceasefire holds, and earnings continue to outperform expectations, allowing the DAX to grind toward the FAZ survey consensus of 25,979 and the Berenberg target range of 25,500–26,200 by year-end, broadly consistent with a continuation of the post-April recovery rather than a new aggressive leg higher

- BULL CASE (25%) — 27,000 – 28,800: A durable ceasefire, further ECB rate cuts after the June hike prove temporary and accelerating fiscal stimulus from Germany's infrastructure and defence programmes push the DAX decisively past its March high, reaching DZ Bank's 27,500 target and potentially the technical analysts' extended target of 28,800.

- BEAR CASE (25%) — 21,000 – 23,500: The ceasefire falters, or US tariff pressure on German autos and industrials intensifies again, while the ECB is forced into further hikes that the fragile German economy cannot absorb. Technical analysts have flagged the 23,500–24,000 zone as the critical support area; a confirmed break could open a retest of the April low near 21,900 or even the 20,500 area where the 2022 uptrend originates.

- DAX forecast 2027: Most institutional forecasts extend the current consolidation-with-upward-bias pattern into 2027 rather than projecting a fresh acceleration. TradersUnion's statistical model places the DAX around 27,881 by end-2029, implying a steady multi-year climb rather than a sharp 2027 breakout. The key swing factor remains the same one driving 2026: whether US trade policy stabilises enough for German exporters — particularly the automotive sector — to plan around a fixed tariff regime rather than continuing to absorb shifting threats.

- Next 5 Years — DAX to 2030 and Beyond: Longer-term forecasts remain broadly constructive. The Association of Technical Analysts of Germany — point toward 28,800 as an achievable medium-term target, while TradersUnion's model projects an average of approximately 33,152 by 2036. The structural case rests on continued fiscal spending under Germany's infrastructure and defence investment programmes, gradual ECB policy normalisation, and the DAX's distinctive global revenue exposure, which insulates the index from purely domestic German economic weakness. The primary long-term risk is a deeper structural decline in German export competitiveness, particularly in the automotive sector, which several 2026 reports already flag as facing dual headwinds from US tariffs and the broader EV transition.

DAX 40 Fundamental Analysis 2026

The DAX's 2026 story is one of resilience tested twice — first by a historic breakout and pullback cycle in Q1, then by an external trade-policy shock in Q2 — against a backdrop of structurally supportive but increasingly complicated monetary policy.

The US Tariff Shock and German Export Exposure

The defining fundamental event of H1 2026 was the imposition of US tariffs on EU goods, ultimately settling at a 15% baseline rate with steeper sector-specific levies on steel, aluminium, and automobiles. The impact has been significant and broad-based: German exports to the US declined by 7.8% over the past year, with machinery and chemical exports falling sharply alongside the more widely reported automotive pressure.

Large German corporates with substantial dollar-denominated revenues have also lost the favourable currency tailwind that supported margins in prior years, as the euro has strengthened against the dollar through 2026. This combination — lower export volumes and a less favourable FX translation — explains why earnings growth expectations for 2026, while still positive, remain vulnerable to downward revision even as headline index levels recover.

The ECB's Hawkish Pivot

On June 12, 2026, the European Central Bank delivered a 25 basis point hike to its deposit rate, taking it to 2.25% — its first hike since 2023. The move was driven by inflation concerns tied to the Strait of Hormuz conflict's impact on energy costs, with the ECB simultaneously raising its 2026 inflation forecast to 3.0% (from 2.6%) while cutting its GDP growth forecast to 0.8%.

For equity markets, this represents a meaningful shift from the easing bias that had supported European equities through most of 2025 and early 2026 — historically, indices like the DAX have benefited disproportionately from monetary easing phases, and a sustained hiking cycle would remove a key structural tailwind, even as the immediate market reaction to the ceasefire news has so far outweighed the rate-hike headwind.

Fiscal Stimulus and the Infrastructure/Defence Programme

Germany's substantial fiscal spending programme — encompassing infrastructure, defence, and climate-related investment funds — remains one of the most important structural supports for the DAX. Consensus 2026 German GDP growth estimates cluster between 0.7% and 1.6%, but importantly, a meaningful share of this expansion is not organic: roughly one-third stems from calendar effects (more working days in 2026), with another significant portion directly attributable to government spending.

Defence spending has translated into long-term contracts and revenue visibility for German industrial and engineering firms, a dynamic that has directly benefited DAX heavyweights like Rheinmetall, which led all 2025 performers with approximately 150% gains on booming European defence budgets.

Global Revenue Exposure — The DAX's Structural Advantage

A frequently underappreciated feature of the DAX is that most of its constituent companies are large multinationals generating most of their revenue outside Germany. This global exposure is the primary reason the index has continued setting records even as German domestic consumer sentiment remains negative — once volatile sectors like autos are excluded, German industrial production, exports, and business expectations have shown signs of stabilisation that headline consumer surveys do not capture.

This decoupling between index performance and domestic economic sentiment is likely to persist as long as German corporates' international revenue base remains intact, though it also means the DAX is more exposed to global trade policy shocks (like the 2026 US tariffs) than to purely domestic German developments.

Energy Prices and the Iran Ceasefire

Lower energy prices have been a persistent tailwind for German industrials and automakers throughout the DAX's multi-year rally, given the country's historically high energy dependence. The reported US–Iran ceasefire — with signing expected in Switzerland on the 19th of June and the Strait of Hormuz set to reopen the same day — has already pushed oil prices to a two-month low, providing renewed relief for Germany's energy-intensive sectors.

However, as with the EUR/USD and broader European equity picture, the durability of this relief depends on the ceasefire holding through implementation, with the ECB's own commentary suggesting energy-driven inflation relief will take months to materialise even in a best-case scenario.

Discover Top German Stocks to Watch Now

DAX 40 Technical Analysis

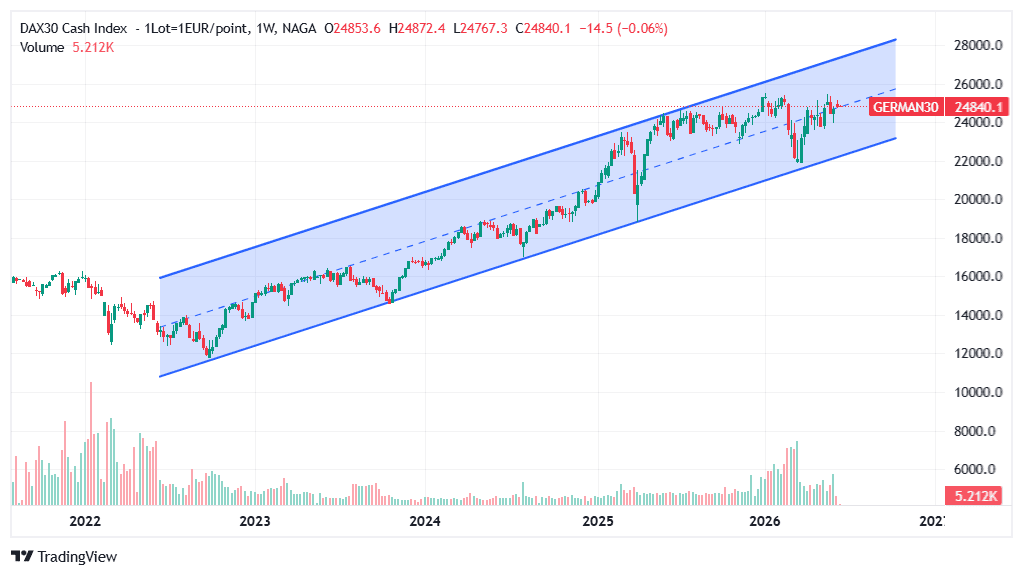

Technically, the DAX's entire post-2022 history can be read through a single dominant structure: a well-defined ascending channel that began forming in Q4 2022, off the energy-crisis low near 11,862. The channel's lower boundary connects that 2022 low through the subsequent higher lows of 2023 and 2024, while the upper boundary tracks the sequence of highs culminating in the January–March 2026 push toward roughly 25,700–26,000.

Past performance is not a reliable indicator of future results. All historical data, including but not limited to returns, volatility, and other performance metrics, should not be construed as a guarantee of future performance.

The bullish 27,000–28,800 target zone sits on the channel's upper boundary as it projects forward through H2 2026 — making it the next dynamic resistance level the index would need to overcome, not just a round-number aspiration.

This channel structure also maps directly onto the three DAX30 H2 2026 scenarios outlined earlier:

- a consolidation within the channel to “meet” the dynamic support by year-end

- a deeper correction toward the lower boundary, around 21,000–23,500

- a push toward the upper boundary, around 27,000–28,800

The channel encodes the same base/bull/bear structure as the fundamental forecasts, which is a meaningful confluence.

Key Technical Levels

LEVEL POINTS SIGNIFICANCE Channel Upper Boundary (H2 2026) ~27,000 – 28,800 Upper rail of the Q4 2022 ascending channel projected through year-end; aligns with DZ Bank's 27,500 target and the technicians' extended 28,800 target 2026 High ~25,700 March 2026 peak; near the channel midline at the time, not yet a test of the upper rail ⬤ Current / Psychological Level ~ 25,000 Sits comfortably inside the channel, below the midline-to-upper-rail zone R2 Pivot / FAZ Consensus 26,181 / 25,979 Classic pivot resistance; broadly aligned with the 29-institution survey average for year-end 2026 Channel Lower Boundary (Rising Support) ~21,900 and climbing The rising trendline tested almost exactly by April's tariff-shock low Channel Origin / Structural Floor 11,862 (Sep 2022) The 2022 energy crisis low before the uptrend started Past performance is not a reliable indicator of future results. Technical levels are analytical reference points, not guaranteed price targets.

To learn more about technical analysis as a forecasting tool, visit NAGA Academy.

DAX 40 Forecast 2026 — Institution Predictions

Here is where Germany's leading banks and the broader institutional consensus stand on the DAX for the rest of 2026:

INSTITUTION END-2026 TARGET BIAS KEY DRIVERS DZ Bank 27,500 Most bullish major bank Fiscal spending cushioning tariffs, inflation under 2%, strong industrials/tech/finance earnings FAZ Survey (29 institutions) 25,979 (average) Bullish consensus Balances US outperformance against German recovery via defence/infrastructure investment Berenberg Bank 25,500–26,200 Moderately bullish Mid-2026 extension on earnings momentum and German recovery signals Leverage Shares 26,000+ Bullish 0.9–1.6% GDP growth, ECB holds/cuts, corporate buybacks supporting rate-sensitive sectors Deutsche Bank 25,000 (consolidation) Most conservative major bank Earnings must exceed expectations to surpass 25,000; 1.5% GDP growth aiding cyclicals TradersUnion (statistical model) 25,892 (average forecast) Neutral, model-based Range of 25,393–26,429; extends to 27,882 by 2029 in long-term projection Forecasts reflect each institution's most recently published figures and may predate the full market repricing following the April tariff shock and the reported June ceasefire. Past performance is not a reliable indicator of future results.

DZ Bank — 27,500, the Bullish Outlier

DZ Bank holds the most bullish target among major German banks at 27,500 by year-end 2026, built on a thesis that fiscal spending provides a meaningful cushion against US tariff pressure, that inflation remains controlled under 2%, and that earnings across industrials, technology, and financial sectors continue to outperform amid a broadly neutral ECB/Fed rate environment. The bank's framework was published before the full extent of the April tariff shock and the ECB's subsequent hawkish June pivot, both of which represent meaningful tests of the underlying assumptions.

FAZ Survey Consensus — 25,979 Across 29 Institutions

The Frankfurter Allgemeine Zeitung's survey of 29 financial institutions produces an average year-end target of 25,979 — arguably the single most representative read of broad institutional sentiment, since it aggregates across banks with otherwise divergent individual views. The consensus explicitly balances expectations of continued US equity market outperformance against a gradual German domestic recovery driven by defence and infrastructure investment, landing on a target that implies modest further gains from current levels rather than a dramatic re-rating in either direction.

Deutsche Bank — 25,000, the Conservative Case

Deutsche Bank's house view is the most conservative among major banks, forecasting consolidation around 25,000 points rather than further substantial gains. The bank's framework emphasises that earnings need to meaningfully exceed current expectations for the index to sustainably trade above 25,000, with 1.5% German GDP growth providing support primarily to cyclical sectors like financials and IT rather than across the broader index.

AI-Based DAX Forecasts — What the Algorithms Say

Algorithmic and AI-driven forecasting models for the DAX show considerably more divergence than the bank consensus above, reflecting the index's genuinely volatile 2026 price action and the difficulty these models have had reconciling the tariff-shock-and-recovery pattern with their underlying historical training data.

MODEL MOST RECENT UPDATE END-2026 TARGET BIAS Long Forecast May 1, 2026 26,197 Bullish, momentum-based CoinPriceForecast February 2026 27,539 Bullish, conservative vs. bank bulls TradersUnion (statistical) June 2026 25,892 (avg); range 25,393–26,429 Neutral-bullish Traders Union (alt. AI model cited Feb 2026) February 2026 29,924 Most extreme algorithmic outlier

The Long Forecast trajectory is the most instructive illustration of how violently these models have swung through 2026. Its April 21 update — published immediately after the worst of the US tariff shock — projected a year-end close of just 21,872, implying a roughly 13.5% decline from the January opening level, as the macro-regression framework weighted the unresolved trade conflict heavily. Just over two weeks later, the May 7 update had already revised this up to 25,193, reflecting improving sentiment after reports that the US and Iran were close to a ceasefire agreement. The most recent May 1 snapshot settled at 26,197, broadly in line with the bank consensus.

This pattern — large swings in algorithmic targets tracking real-time news flow rather than slower-moving fundamentals — is a useful reminder that AI/statistical models can be more reactive than predictive in genuinely volatile macro environments and are best read as a real-time sentiment gauge alongside, rather than instead of, fundamental bank research.

DAX Price History — Key Moments

The DAX's modern history is a story of accelerating milestones: the journey from 5,000 to 10,000 points took more than 16 years, while recent round-number thresholds have fallen in a fraction of that time — a reflection of both genuine earnings growth and the index's increasingly global revenue base.

September 2022: The Energy Crisis Low

Russia's invasion of Ukraine and the resulting European energy crisis drove the DAX to a multi-year low near 11,862 in September 2022, as soaring gas prices and recession fears weighed heavily on Germany's energy-intensive industrial base. This low marks the starting point of the multi-year uptrend that has driven the index to its subsequent record highs.

May 20, 2025: 24,000 for the First Time

The DAX crossed 24,000 points for the first time in its history on May 20, 2025, reaching an intraday high of 24,079.40. The breakthrough was driven by easing US-China trade tensions, strong corporate earnings (particularly from SAP, Siemens, and BMW), and growing market expectations of ECB rate cuts in the second half of 2025.

January 7, 2026: The Historic 25,000 Breakout

The DAX surpassed 25,000 points for the first time in its history on January 7, 2026, touching an intraday high of 25,003.73 in the first minutes of trading. The milestone was driven by expectations of a 2026 German economic upturn fuelled by multi-billion-euro government investments in infrastructure and defence, alongside expectations of lower global oil prices easing inflationary pressure. Notably, only two of the 40 index constituents — Heidelberg Materials and Siemens Energy — were themselves trading at individual record highs at the time, highlighting how concentrated the rally's underlying drivers were.

March 2026: Extension to 25,700 and Technical Buy Signals

Building on 34 separate all-time highs recorded in 2025 and further records in early 2026, the DAX extended to roughly 25,700 by March, a level that prominent German technical analysts flagged as confirming a strong long-term buy signal, with extended targets of 27,200 and 28,800 floated for the year. Even at the time, however, analysts cautioned that 2026 would not pass without corrections, specifically flagging spring and autumn as likely periods of weakness.

April 2026: The US Tariff Shock

The DAX's sharpest 2026 reversal came in April, as the United States imposed a 15% baseline tariff on most EU goods entering the country, with steeper sector-specific levies on steel, aluminium, and automobiles. German exports to the US fell 7.8% over the following months, and the DAX retreated to roughly 21,900 — erasing the bulk of the year's gains and decisively testing, though not breaking, the broader multi-year uptrend.

June 2026: The Ceasefire Recovery

Following a sharp single-session selloff of 1.31% on June 3 (which brought the index to roughly 24,796 amid fading Middle East ceasefire hopes and fresh tariff threats), the DAX staged a steady recovery as reports of an imminent US–Iran ceasefire — with signing expected in Switzerland and the Strait of Hormuz set to reopen the same day — lifted European equities broadly. By June 16, the index had recovered to approximately 24,910, briefly crossing 25,000 intraday, with Europe's broader STOXX 600 index hitting its own record high on the news just one day earlier.

When looking for DAX price predictions, it is important to remember that analysts' forecasts can be wrong, sometimes substantially, as the wide divergence between AI models published just weeks apart in 2026 demonstrates. Projections are based on fundamental and technical analysis of historical price movements; past performance and forecasts are not reliable indicators of future results. It is essential to conduct your own research. Your decision to trade depends on your attitude to risk, your expertise in the market, the spread of your investment portfolio, and how comfortable you feel about losing money. Never invest money you cannot afford to lose.

Sources:

- Trading Economics — Germany Stock Market Index (DE40)

- European Central Bank — Monetary Policy Decisions, June 12, 2026

- IG International — DAX 40 Market Outlook 2026

- Capital.com — Germany 40 (DAX) Forecast Updates

- Frankfurter Allgemeine Zeitung — Institutional Survey

- Deutsche Börse — DAX Index Data & Surveys

Other Resources

- Dow Jones forecast & price predictions 2026

- NASDAQ 100 forecast & price predictions 2026

- EUR/USD forecast & price predictions 2026

- Oil forecast & price predictions 2026

- Natural Gas forecast & price predictions 2026

- Gold forecast & price predictions 2026

- Silver forecast & price predictions 2026

- IBEX 35 forecast & price predictions 2026

- German Stock Market Academy Guide

- How to trade stocks and indices