The biggest news in the past 24 hours has, without a doubt, been the Japanese currency intervention! The intervention caused the USD/JPY to decline by 556 PIPs or 3.82%. The price has since increased again back up to 142.140. Of course, the price has not changed much since the retracement, but the Japanese government had most likely acted to avoid the exchange rate reaching close to 150.00.

US Indices

The US stock market is experiencing its fourth consecutive day of declines. The price has declined by 3.20% this week which is a considerable amount. Investors will concentrate on the most recent support level which was formed in June 2022. At this level, will the price form a bearish breakout or find support? Investors will also soon turn their attention to the quarterly earnings reports which are scheduled for October and November.

Crude Oil

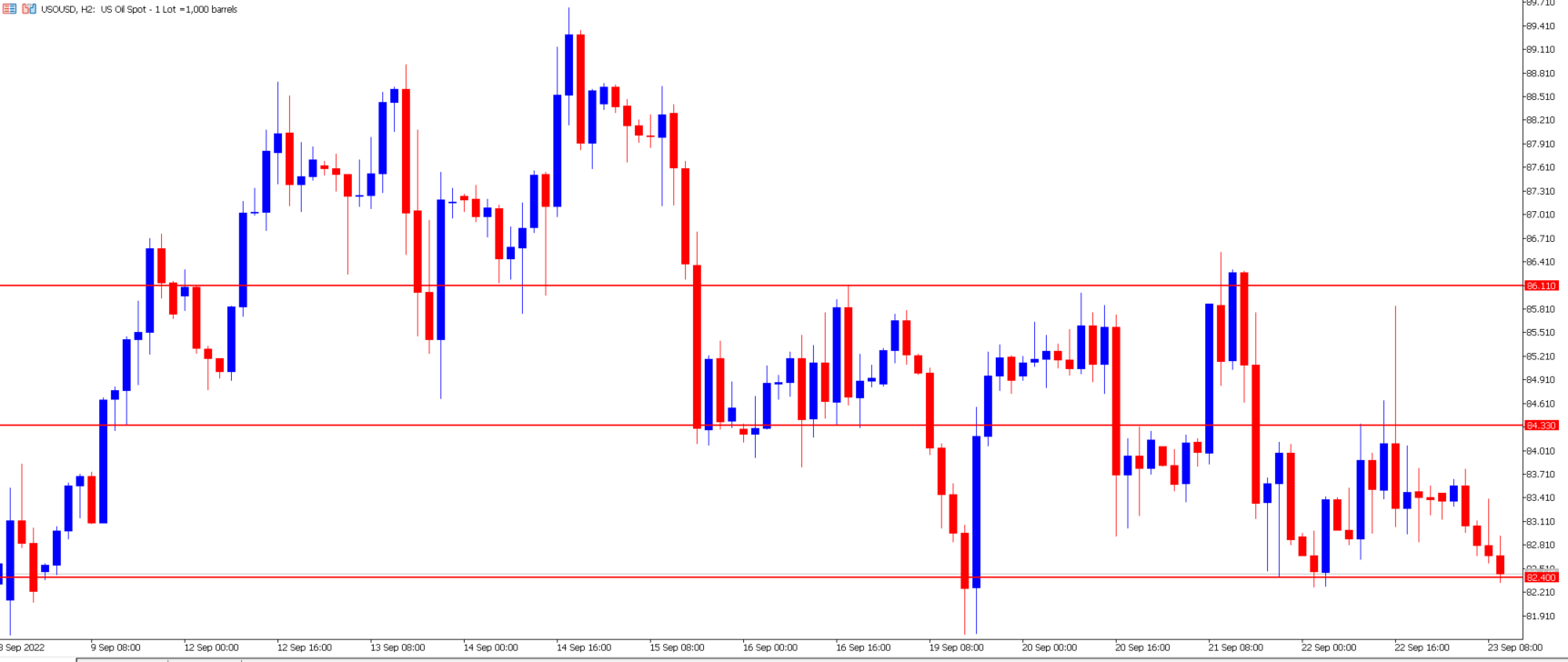

The price of crude oil is mainly trading within a recurring price range with any attempted breakout collapsing and returning to the range. The current range is $84.33 and $82.40. Another strong resistance point can also be seen at $86.11 and can create a further price range.

Crude Oil 2-hour chart on September 23rd

The price of crude oil is currently being influenced by two major factors. The first is the monetary policy tightening - not only in the US, but across global economies. The move is aimed at lowering prices, this includes crude oil. However, prices were also supported by the recovery in demand for oil in China and Japan, as well as the growth of geopolitical risks.

The latest reports from China advise that many large government-owned and private refineries are considering increasing production by up to 10% over the next month. This decision has most likely been taken in anticipation of stronger demand and a possible increase in fuel exports in the last quarter of this year. The effect on the price will depend on the level of increased demand vs increased production.

USD/JPY

USD/JPY 1-hour chart on September 23rd

The price of the USD/JPY pair will continue to be influenced by the restrictive policy being imposed by the Federal Reserve, as well as indications given during the press conference. There seems to be a clear indication that the Central Bank’s stance will not be changed unless inflation declines significantly.

The Central Bank also released their predictions for the next 2 years, confirming that the rise in interest rates will lead to increased pressure on the economy and a lower GDP (Gross Domestic Product). The report indicated that they expect the GDP to drop by 0.2%, and to 1.2% next year. Inflation will be able to return to the target level of 2% no earlier than 2025, and rates will begin to slowly decrease no earlier than 2024. The report vanishes any previous opinions regarding potential rate cuts in early 2023.

The price of the Japanese Yen significantly declined in the first 3 ½ days as the Bank of Japan refused to amend its monetary policy. BoJ is the only Central Bank that has avoided increasing interest rates, insisting that, “we will not increase rates just because everyone else is”. However, this has had a negative effect on the Yen and has now forced the finance ministry to intervene in the currency for the first time since 1998. The Governor of the BoJ has advised that he believes the level of inflation will decline in the early month of 2023 without policy alteration.

The currency intervention has caused the Yen to increase in value but the currency still remains very weak. Most economists have advised that currency interventions have not worked in the past and are not likely to work in the long run.

Quick Summary:

- Japan intervenes in the exchange rate for the first time in almost 25 years.

- USD/JPY declines by up to 3.82% following the announcement.

- BoJ refuses to increase interest rates, counting on inflation declining in 2023.

- Fed predicts a lower GDP for the next 2 years and predicts no rate cuts for 2023.

- US indices decline for a fourth consecutive day and reach support level.