The stock market improved after declining for four consecutive days due to high bond yields and poor employment data. However, technical analysts indicate that most indices' prices remain below longer-term Regression Channels and Moving Averages. Fundamental Analysts also point out that bond yields remain high, and interest rate hikes are likely this year. This morning, the price of the SNP500, Dow Jones and NASDAQ has dropped below the Volume-Weighted Average Price.

Therefore, investors should still be aware a further downward price movement is possible. However, this depends mainly on tomorrow's official employment and US inflation data. This morning, the US 10-year Treasury Bond Yields are again increasing by 0.14%. If bond yields continue to rise throughout the day, the stock market will likely correct previous lows.

The US Dollar Index declined during yesterday’s trading session and is trading slightly lower this morning. However, investors should note that the Dollar’s price action is improving as the European Cash Market opens. The best-performing currency, if we exclude the earning Asian session, is the US Dollar and the Euro. The weakest currency has been the Japanese Yen and the Swiss Franc.

NASDAQ

The NASDAQ is trading 0.25% lower than the day’s open price and is declining similarly to European equities. The NASDAQ significantly rose in value yesterday, increasing by 1.36%, and continues to trade within the price range formed on September 22nd. Analysts are advising investors have priced the asset within this range, which is unlikely to change until the US NFP and Inflation data have been released. If the employment data is more robust than previous expectations, the NASDAQ and US equities will likely experience further pressure.

Analysts expect tomorrow’s Non-Farm Payroll to read 170,000, the lowest we have seen in over 12 months. The Unemployment Rate is believed to decline from 3.8% to 3.7%, and the Average Hourly Earnings are expected to rise from 0.2% to 0.3%. If the NFP and Average Hourly Earnings read higher than expectations while the Unemployment rate declines, investors will struggle to hold onto their “long” positions. A more resilient employment sector will prompt the Federal Reserve to hike this year. As a result, the NASDAQ and other indices potentially can decline.

Employment data so far this week have yet to give a clear picture. The number of new vacancies in August rose from 8.920 million to 9.610. In contrast, analysts expected the data to remain unchanged, which raised investor fears that the regulator would be forced to return to “hawkish” rhetoric. However, yesterday, the mood of experts changed due to the publication of September employment data from the Automatic Data Processing (ADP) company. The number of new jobs adjusted by 89,000, significantly lower than the forecast of 154,000 and the previous value 180,000. However, the Services PMI data read higher than expectations.

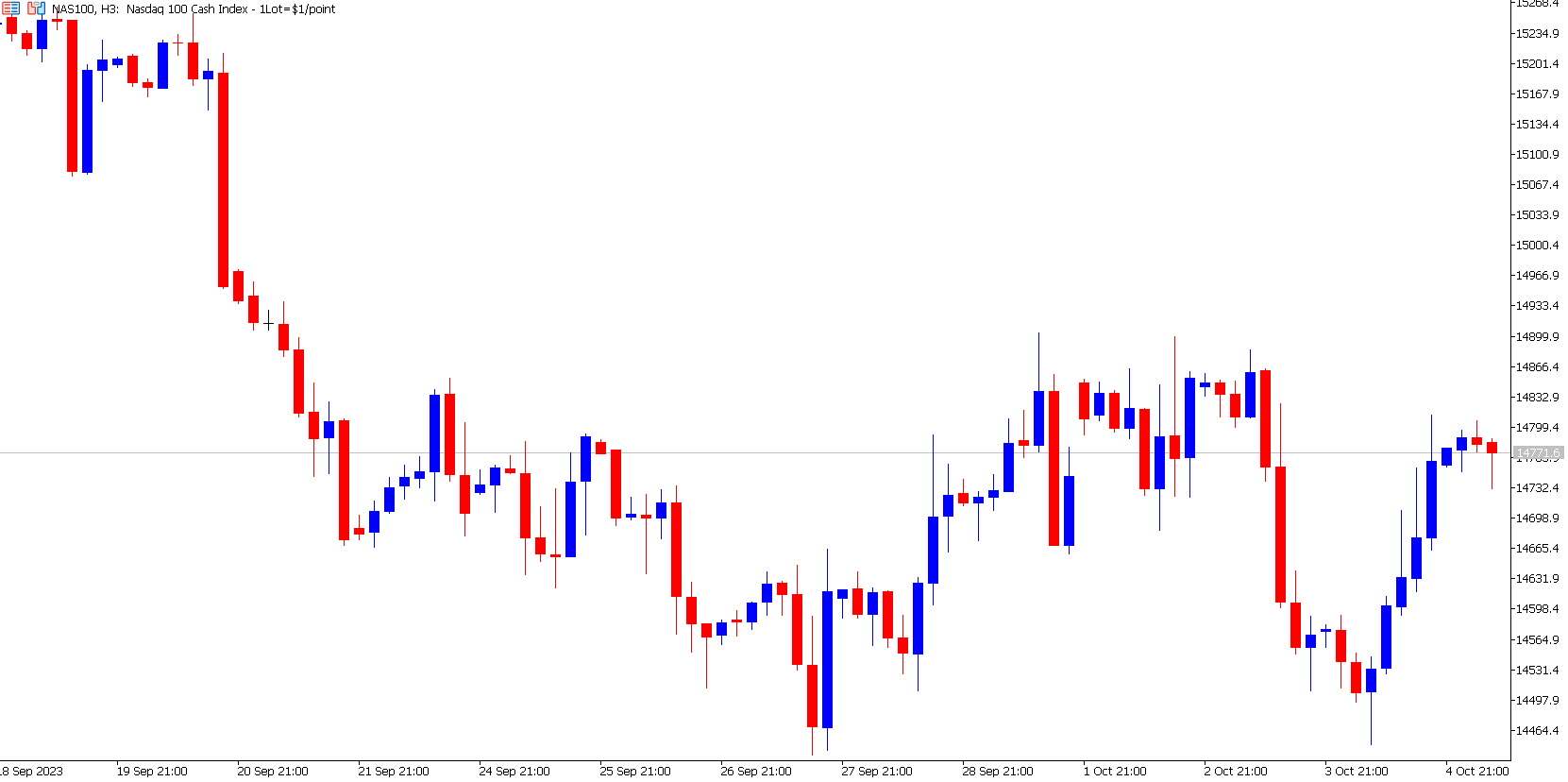

NASDAQ 2-Hour

The NASDAQ is unlikely to move outside the established price range before the employment release tomorrow afternoon. In the meantime, the NASDAQ is trading below the Volume-Weighted average price but is experiencing slightly higher delta statistics. Therefore, signals are contractionary, but EU indices are declining, and the price is lower. Here, the asset is witnessing downward signals, but buyers remain within the market; therefore, an upward impulse wave is possible.

XAU/USD

The price of Gold is experiencing significantly lower volatility levels than other assets, including the Dollar and equities. However, this is primarily due to the sharp decline and the instrument declining for eight consecutive days. The commodity has declined almost 6% since September 19th. Gold is a safe haven asset competing against bonds and the US Dollar. Strong correlations can be seen here between assets within the safe haven category. The poor performance of Gold is primarily due to the high bond yields, restrictive monetary policy and expensive Dollars. The rise in bond yields can also be seen in the EU, where German 10-year bonds are trading at 3.000% for the first time since 2011. This suggests that markets expect interest rates to remain at high levels longer.

Technical analysis indicates that the commodity's price will remain within the price range and experience reverting waves. However, this will likely change after tomorrow’s employment data is publicised. Once the Federal Reserve and Central bank are forced to halt any further interest rate hikes, Gold will be able to regain bullish dominance, particularly if investors look to purchase the discounted price. As the price is trading within a range, if the price breaks above $1,829, traders should be cautious of a false breakout. Therefore, the price potentially may retrace back to the previous range.

Summary:

- The stock market improved after declining for four consecutive days due to high bond yields and poor employment data.

- The stock market is likely to remain within its current range until the announcement of the latest US employment data. Bond yields are still a concern for shareholders, but lower employment data can boost the stock market.

- Gold is experiencing lower volatility levels than other assets, including the Dollar and equities. However, this is primarily due to the sharp decline and the instrument declining for eight consecutive days.

- Gold requires the current interest rate hiking cycle to halt in order to obtain serious longer-term buyers.

- Only 2 of the 10 most influential stocks within the NASDAQ are increasing in value in this morning’s pre-market open.