The Bank of England announced that the UK economy is likely to fall into a deep recession which has caused the British Pound to decline significantly against most currencies. Yesterday, the price of the GBP/USD declined by 2% and by 1.40% against the Euro, even as the regulator hiked a further 0.75%. However, investors took advantage of the weaker Pound to invest in UK stocks. The FTSE100 increased by 0.75% after the Pound significantly weakened.

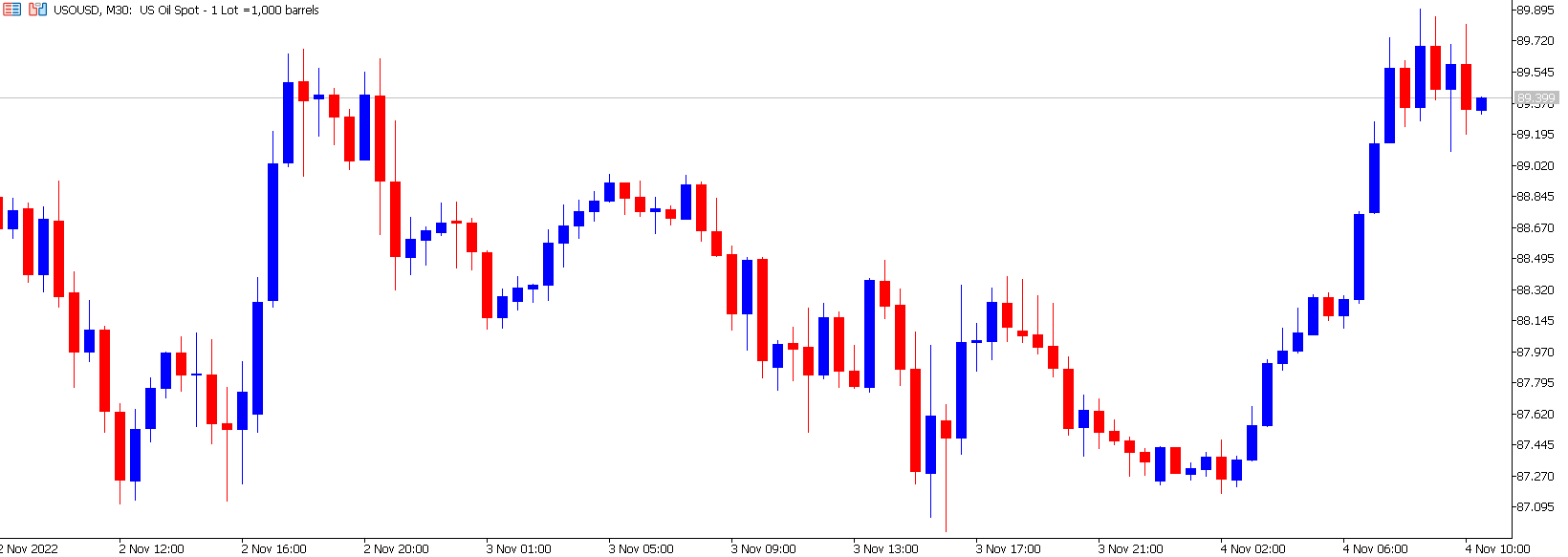

Crude oil, on the other hand, seems to be ignoring the stronger US Dollar and jumbo rate hikes, which normally triggers a decline in its price. Crude oil significantly increased in value during this morning’s Asian session climbing to almost $90 per barrel. The price action is currently measuring a 3% increase but traders are cautious that the price may struggle above $90 per barrel. $90 per barrel is known to be a significant psychological level for buyers.

The main driver for the price of oil has been the significantly lower crude oil inventories as well as the unexpected high consumer demand. The latest crude oil inventories decreased by 3.115 million barrels and gasoline by 1.257 million barrels, whereas the sales figures continue to remain high and stable.

Crude oil 30-minute chart on November 4th

Furthermore, the price of gold has increased this morning as the US Dollar has retracted slightly. Gold is supported by the current risk of recession but has little room to maneuver while interest rates remain so high. However, economists have advised that the price still has the potential to increase in 2023 if the economy continues to contract and interest rates pivot. Even with the strong decline and high demand for cash, gold still maintains its “safe haven” status.

EUR/USD

The price of the EUR/USD is currently moving within a retracement in favor of the Euro. The price has increased by 0.30% during this morning’s Asian session but still remains lower than yesterday’s price range. Technical indicators are currently signaling a retracement rather than a bullish trend. Based on the indicators, it is too early to determine whether the price will maintain enough momentum to form a higher high. Fundamentals, on the other hand, remain in favor of the USD so far.

EUR/USD 1-hour chart on November 4th

The price of the US Dollar continues to be influenced by Wednesday’s interest rate decision and the Chairman’s forward guidance. According to Chairman Jerome Powells, a smaller rate hike may be appropriate soon but is unlikely to be at the next rate decision in December. However, this will also depend on today’s employment figures (NFP) and next week’s inflation rate (CPI).

This makes the upcoming NFP figure and unemployment rate extremely important. The unemployment rate has remained at all-time-lows over the past few months. Nonetheless, the Non-Farm Payroll (NFP) figure has shown signs of significant slowdown. If figures improve as the JOLTS Job Openings did, it may support the theory of higher inflation and a more restrictive policy. This is again positive for the national currency $USD and negative for US stocks.

The head of the ECB, on the other hand, advised that the regulator cannot mimic the actions of the US Fed to combat the current high level of inflation, since the economic conditions in the Eurozone are quite different. The ECB’s dovish tone compared to the Fed is generally putting additional pressure on the currency pair.

Quick Summary:

- The Bank of England increases interest rates by 0.75%, but the Pound continues to struggle.

- The Governor of the Bank of England advises that the UK will fall into a recession.

- Crude oil prices increase in value despite the more expensive US Dollar. Prices supported by lower supply and high stable demand.