Markets have been cruising in a tight range this week, with the S&P 500 hovering just below record highs and European indices like the FTSE 100 holding up thanks to strong energy and bank names. Gold smashing through $4,000/oz grabbed plenty of attention — a clear sign that safe-haven demand isn’t going anywhere. Meanwhile, oil’s up more than 2% since last week’s close, keeping commodities in focus.

So far, the vibe’s steady but cautious. Traders are walking the line between optimism and a fresh wave of geopolitical worries, all while trying to read the tea leaves on U.S. data and global growth. Equities are consolidating, commodities are firm, and everyone’s waiting for that next catalyst to shake things loose.

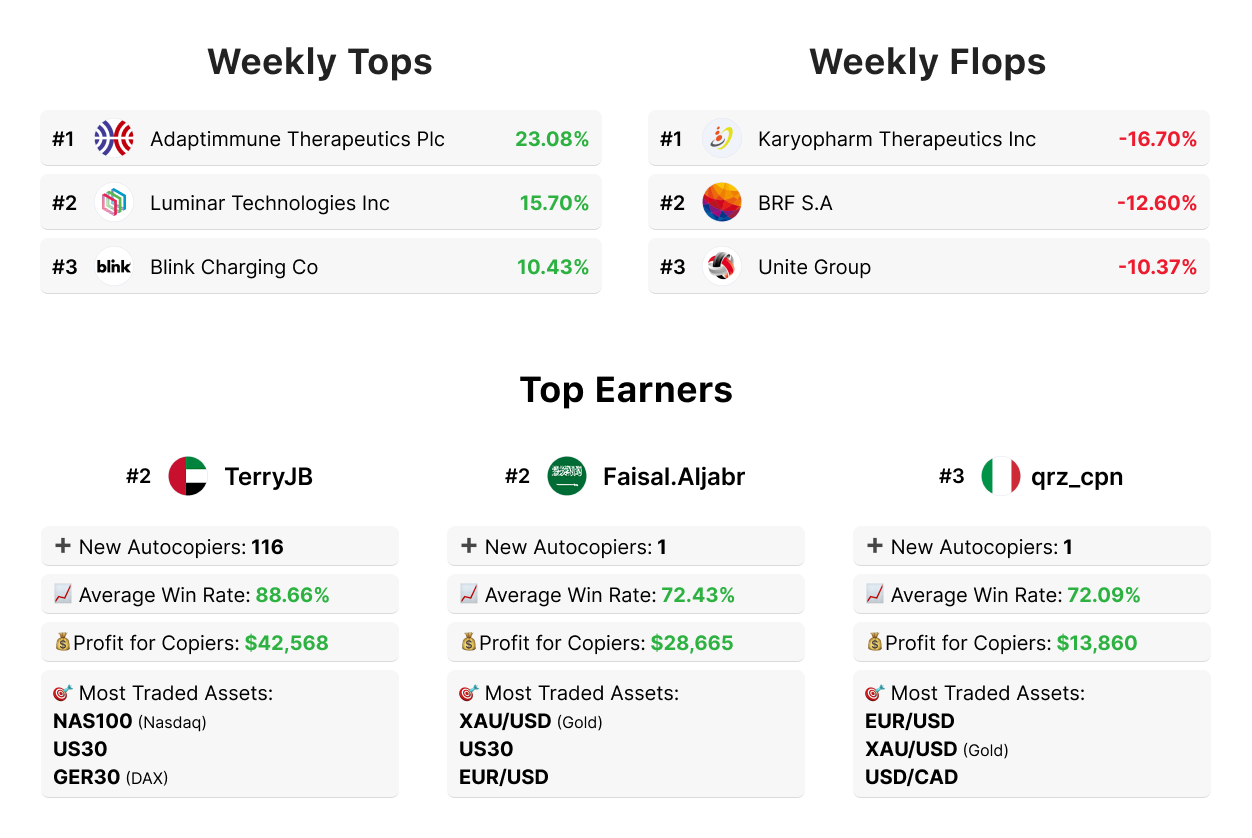

It is important to remember to assess your financial situation and risk tolerance, before engaging in copy trading. Past performance and forecast are not reliable indicators of future results.

Market Overview: Calm on the Surface, Caution Beneath

Markets stayed within a narrow range this week as traders balanced optimism with lingering risks. Oil’s rebound and renewed geopolitical tensions kept commodities and inflation expectations in the spotlight.

In Europe, indices found support from a weaker euro and firm energy prices, while investors kept a defensive stance ahead of upcoming policy updates and macro data. For now, the tone across markets remains steady—but fragile.

*Trading involves significant risk of loss.

Tech Strength Meets Cautious Optimism

The S&P 500 hovered near record highs this week, powered by large-cap tech and steady financials. Across the Atlantic, the FTSE 100 extended its momentum, lifted by gains in energy majors and banks.

Despite the firm backdrop, traders continue to watch for signs of inflation volatility or geopolitical shocks that could challenge recent equity resilience. For now, dip-buying remains the strategy—but patience is the mood.

*Trading involves significant risk of loss.

Gold Shines, Oil Finds Its Footing

Gold broke above $4,000/oz for the first time this week, marking a historic milestone driven by safe-haven demand and lower yields. Meanwhile, oil prices climbed roughly 2%, supported by improving demand expectations and OPEC+ production discipline.

The dual rally underscores a cautious but active commodities market—one where traders are hedging against uncertainty even as growth sentiment tries to stabilize.

*Trading involves significant risk of loss.

Dollar Dominates, Yen Hits New Lows

The U.S. dollar stayed firm, supported by resilient yields and risk-off positioning. The euro remained under pressure after weak regional data, while USD/JPY surged to its highest level since February, reflecting the ongoing divergence in BoJ policy.

Sterling traded sideways, and commodity currencies like the Aussie and loonie gained modestly on oil’s strength. Ahead of next week’s U.S. inflation data, traders are staying nimble—ready for volatility to return.

*Trading involves significant risk of loss.